The Inside Story Of How The Ricketts Family Schemed And Feuded Their Way To Owning The Chicago Cubs

On October 27, 2009, the Ricketts family officially purchased a 95 percent ownership stake in the Chicago Cubs from the Tribune Company, bringing an end to a long, arduous, and complex sale process. Now, thanks to a cache of emails and documents obtained by Deadspin, more details from that process can be revealed than ever before, providing an unprecedented insider’s view of an MLB team sale.

The Cubs were officially put up for sale shortly after billionaire Sam Zell purchased the team’s parent company, the Tribune Co., in April 2007. Zell took control through a leveraged buyout—a technique that allows the buyer to borrow heavily in order to make a purchase and then saddle the existing company being purchased with the resulting debt—worth $8.2 billion, leaving the Tribune with $13 billion in total debt. Once the purchase was complete, Zell went about completing the second step of the leveraged buyout playbook: stripping the acquired company down to the studs and selling off whatever assets still hold value. Thus, the Cubs were suddenly for sale.

The documents and emails below come from the inbox of Joe Ricketts, founder of TD Ameritrade and billionaire patriarch of the Ricketts family. Though his son Tom led the family’s efforts throughout the sale process, the emails reveal that Joe, whose wealth bankrolled a significant portion of the purchase, kept close watch on the negotiations and was looped in on major decisions. Scores of conference-call notes, financial analyses, bid presentations, and other documents and updates related to the sale found their way into Joe’s inbox.

The Ricketts family were one of the first bidders to pursue the Cubs, and by the summer of 2008 Joe Ricketts was regularly receiving updates about “Project North Side,” which is what the family codenamed their quest for the team.

These emails depict the purchase process as a herculean task, spanning years and requiring the efforts of an ever-expanding cast of lawyers, consultants, and bankers. They reveal new details about the tax-dodging particulars of the sale and a near deal-wrecking amount of late-stage animosity between the Ricketts and the Tribune, and provide further insight into the exploding value of MLB franchises, and how that explosion has changed what it means to own and root for a baseball team.

Additionally, they reveal a fair amount of intra-family squabbling, much of it genuinely tense. This is revealing not just for the broad insight it gives into the workings of one of America’s foremost political families— one that happens to operate like a business—but more narrowly for how it shows the would-be owners of one of America’s most famous sports franchises jockeying to use the purchase to burnish their own personal brands. Teams are businesses; they are also mechanisms the rich and powerful use to project their images and stroke their egos.

The earliest emails come from July 2008, right when the Ricketts’ pursuit of the Cubs started to kick into high gear, and run through the entire process of the sale. Excerpts of the most interesting correspondences and documents found within them are laid out below, in chronological order. The full version of every document referenced is linked to for readers to examine. This is the inside story how the Cubs were purchased by the Ricketts family, from beginning to end.

July 1, 2008

Joe Ricketts received an email from an attorney at Foley & Lardner, the law firm the family hired to help shepherd a deal for the Cubs, explaining one of the key components of the Tribune’s sale proposal: the company’s desire to dodge hundreds of millions of dollars in taxes:

All:

I am attaching a confidential memorandum that discusses the seller’s proposed tax structure, which one of our tax partners prepared. The unique structure raises a lot of questions, and the answer to each question tends to raise another question. Therefore, the memorandum is lengthy and not light reading. Please do not hesitate to let us know if you have any questions or other reactions to the memorandum.

Also, there are some potential tax planning opportunities that this memorandum does not address in detail, so it is likely that we will be supplementing the memorandum with additional advice.

Thank you.

Attached to that email was a document titled “outline of tax issues,” which explained exactly how Zell and the Tribune planned to sell the Cubs without having to pay any taxes on the revenue produced by the transaction.

Zell’s plan to pull a fast one on the IRS began with his purchase of the Tribune, when he reclassified the company as an S corporation, a complicated accounting trick that involved altering the Tribune’s shareholder structure to make it exempt from federal income taxes. Selling the Cubs presented a problem, though, because any such sale that took place within 10 years of the S election would expose the Tribune to paying gains taxes. But, as the tax issues memo explained, Zell had another idea for how to solve the problem of paying taxes:

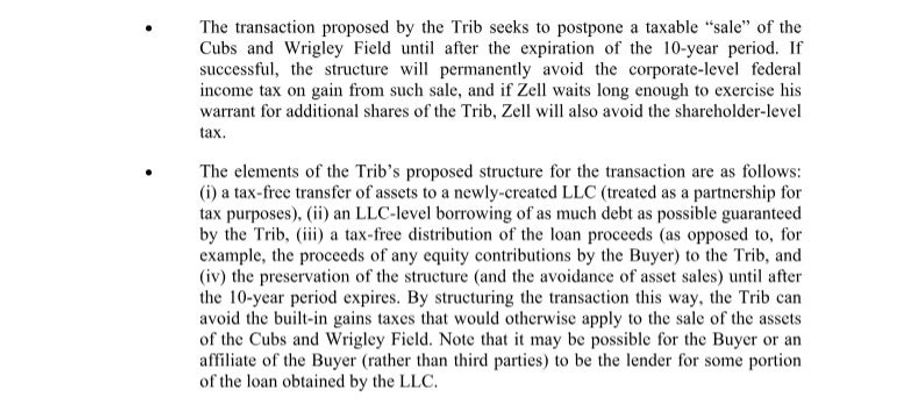

What’s being described here is a leveraged partnership. Under this plan, the Tribune wouldn’t technically sell the Cubs to the Ricketts, but would instead partner with them to form a new limited liability corporation which would own the Cubs and in which the Ricketts would have a controlling stake. Then, the LLC would load itself down with as much debt as possible and funnel the borrowed cash to the Tribune. The Tribune would get cash-rich but remain in debt without ever actually technically selling the Cubs, and the Ricketts would get control of the Cubs without ever actually buying them from the Tribune. Only when the partnership was safely clear of the 10-year window would the Tribune officially sell its remaining stake in the Cubs to the Ricketts.

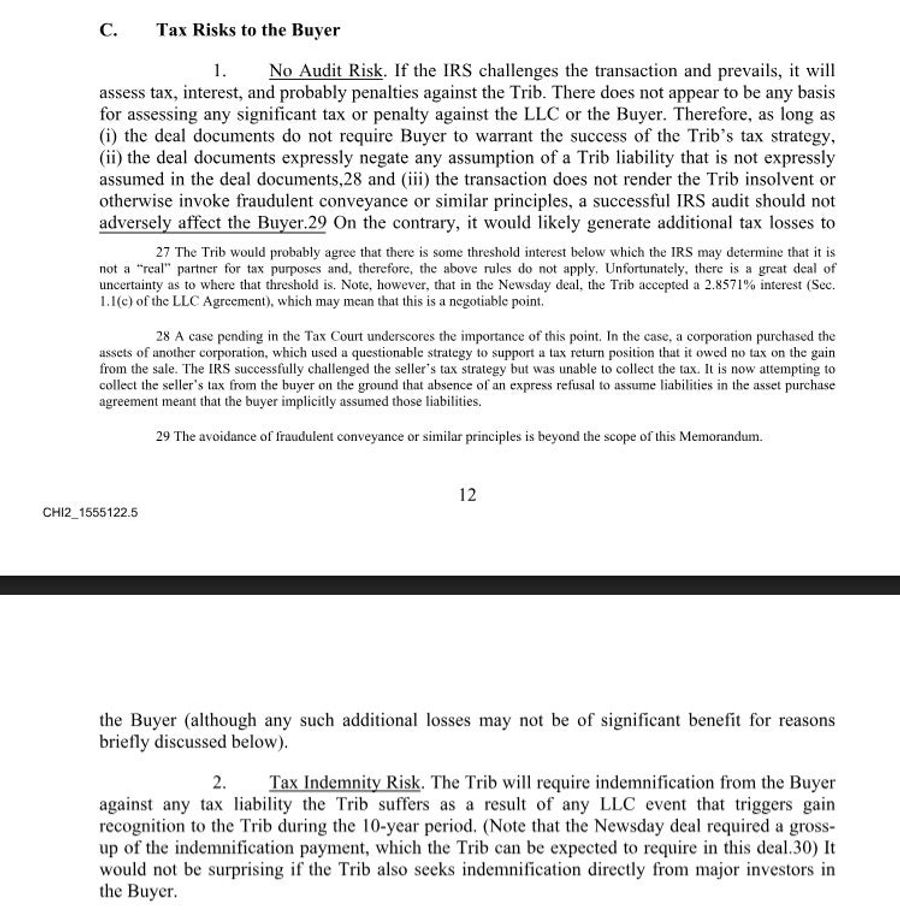

At no point in the tax-issues memo or in any of the Project North Side-related emails that hit Joe Ricketts’ inbox does anyone express any concerns that the Tribune’s scheme was immoral and legally dubious. The memo does mention that the IRS might take issue with the leveraged partnership, but only to assure the Ricketts that they would not be in danger of an audit, and that the Tribune would like to be indemnified should the Ricketts do anything that triggered a gains tax on the new partnership:

This is the same sale structure Zell used when he flipped Newsday, another distressed asset in the Tribune’s portfolio, to Cablevision in 2008, as . Neither sale sat well with the U.S. government, and in 2016 the Tribune agreed to pay a $270 million fine to the IRS in connection with the Newsday sale. The government is currently pursuing legal action against the Tribune, seeking a similar fine in relation to its sale of the Cubs. The case is currently set for trial on Oct. 28, 2019.

A spokesman sent along the following statement on behalf of the Ricketts family in response to questions about their willingness to go along with the Tribune’s tax-dodging plan:

The structure of the transaction was entirely dictated by the Tribune. The Ricketts siblings (Pete, Tom, Laura and Todd) prevailed by adhering to those terms and providing the most compelling bid. The siblings formed the team board of directors with Tom serving as chairman of the board. Joe Ricketts has no role in the operations of the Cubs and derives no financial benefit from the team.

From day one of their ownership, the Ricketts siblings promised they would be good neighbors to the city of Chicago; preserve Wrigley Field for future generations and win a World Series. They have delivered on those promises in every way, from millions of dollars in donations and investments through Cubs Charities, to a billion-dollar investment into Wrigley Field and the neighborhood; to putting together the business and baseball talent to win the 2016 World Series and end a 108-year championship drought.

Sam Zell declined to comment on this story. When asked about the tax-avoiding benefits of the leveraged partnership structure and the IRS’s case against the company, the Tribune referred to comments made in its latest 10-K filing:

We continue to disagree with the IRS’s position that the transaction generated a taxable gain in 2009, the proposed penalty and the IRS’s calculation of the gain. During the third quarter of 2016, we filed a petition in U.S. Tax Court to contest the IRS’s determination. We continue to pursue resolution of this disputed tax matter with the IRS. If the IRS prevails in their position, the gain on the Chicago Cubs Transactions would be deemed to be taxable in 2009. We estimate that the federal and state income taxes would be approximately $225 million before interest and penalties.

In January 2019, the Tribune finally sold their remaining five percent stake in the Chicago Cubs to the Ricketts family.

July 2, 2008

In addition to helping the Tribune avoid taxes, the Ricketts had to start thinking about how they were going to finance their purchase of the Cubs, which came with an initial price tag nearing $1 billion. The Ricketts were going to have to borrow money—a lot of money—in order to make a competitive bid, so Foley & Lardner was dispatched to take a look at MLB’s rules to determine just how much debt the Ricketts could get away with carrying.

MLB teams must comply with the league’s debt service rules, which under the current CBA state that a team cannot carry debt that exceeds eight times its earnings before interest, taxes, depreciation, and amortization (EBITDA). The rules were a little more forgiving back in 2008—the limit was 10 times EBITDA—and a memo prepared by Foley & Lardner, called “MLB rules,” estimated that the Cubs could carry a debt of up to $349 million in 2009 without running afoul of them. The memo expressed bigger concerns, though, about how the Tribune’s tax-avoiding sale structure might complicate things to the point that MLB wouldn’t approve the sale.

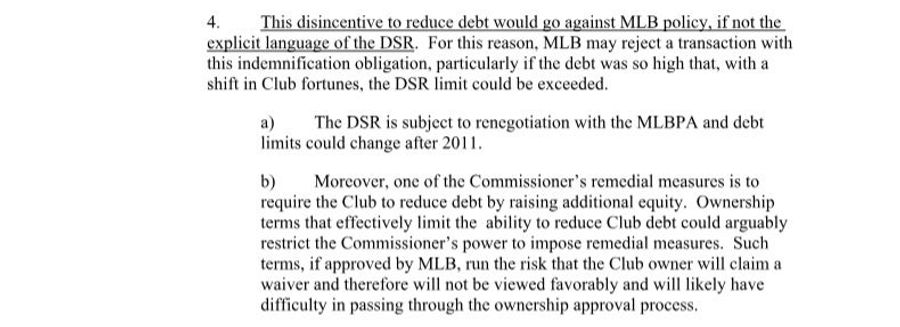

According to the memo, the Tribune’s proposal could potentially cause problems not just because the initial deal would require the team to carry a lot of debt, but because attempts to service that debt might expose the Tribune to tax liability and thus trigger the indemnification clause that would place that liability on the Ricketts. Going by the memo’s analysis, this would put the Ricketts in a paradoxical position: needing to pay down their debt in order to avoid violating MLB rules, but needing to avoid doing so in order to avoid triggering a tax payment. This was described as a seemingly existential threat to the Ricketts’ chances of acquiring the team:

This was more worrying than was necessary. MLB teams—including the Los Angeles Dodgers, New York Mets, Philadelphia Phillies, and Washington Nationals— regularly exceed MLB’s debt limit, and though the penalties for doing so are defined by the CBA, the enforcement of the rules is almost entirely at the discretion of the commissioner. As later documents make clear, the Ricketts were able to acquire the Cubs while carrying much more than $349 million in debt.

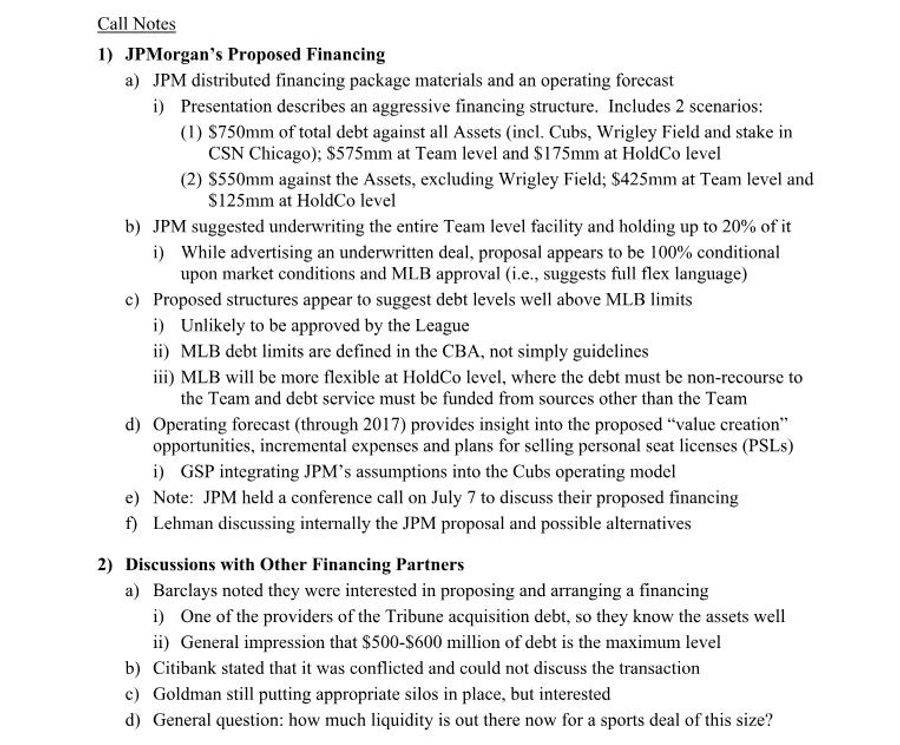

July 7, 2008

Even though it would ultimately prove unimportant, the debt issue remained a headache for those working on Project North Side. Notes from a conference call that included Tom, Pete, and Laura Ricketts and a handful of attorneys and financial advisors reveal that the proposed debt structures provided to them by JPMorgan and other banks went far beyond MLB’s limits.

July 17, 2008

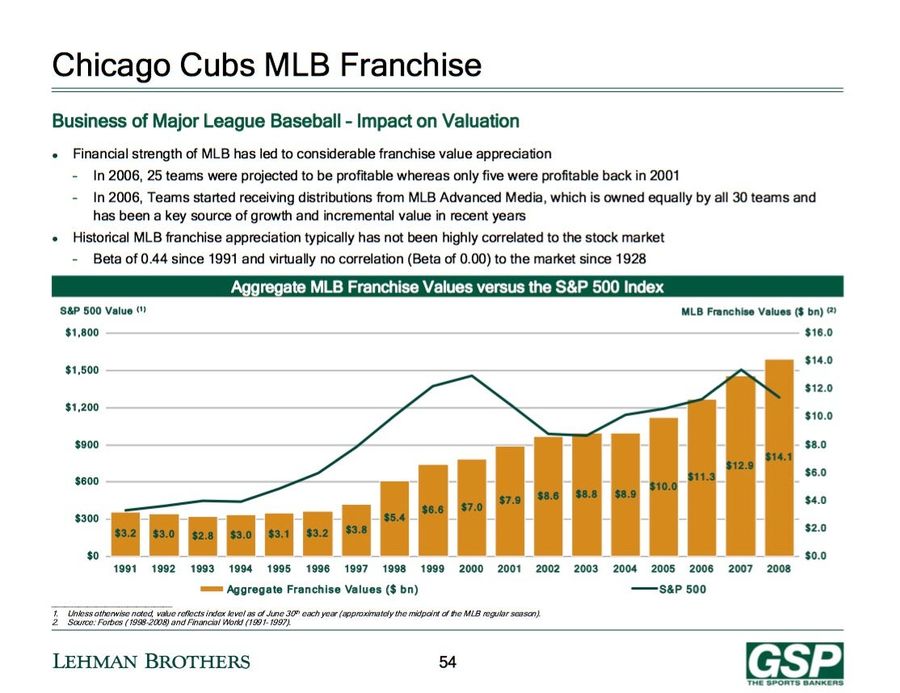

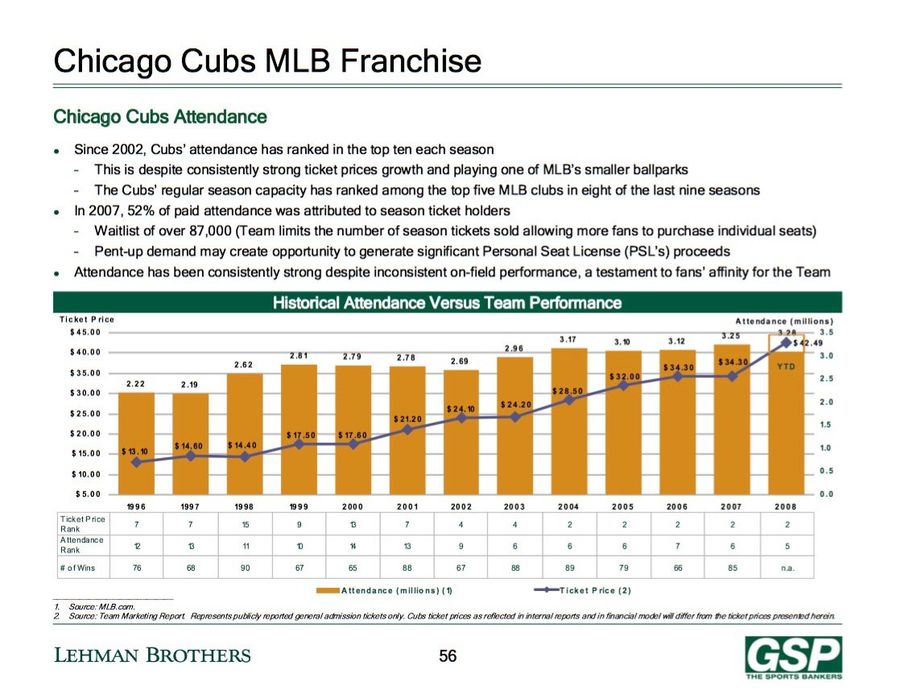

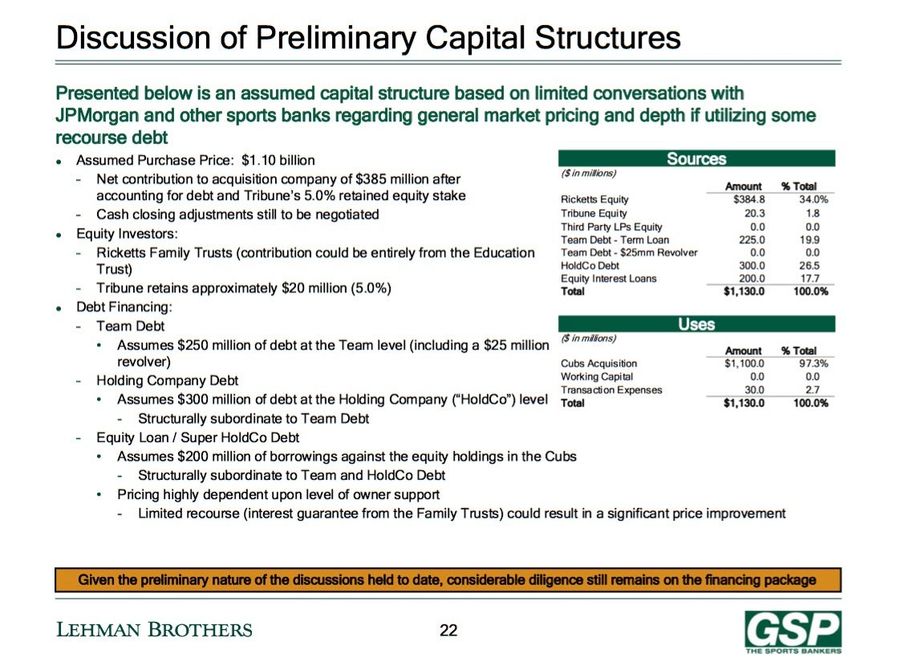

Nevertheless, the Ricketts drove ahead, and the next step was to get an in-depth analysis of just how much the Cubs were actually worth. The family dispatched Galatioto Sports Partners (GSP), a company that consults on pro sports transactions, to prepare an investment analysis. The resulting report, which is 102 pages long, was sent around to the family.

The report’s main conclusion was unsurprising: The Cubs represented a bulletproof investment opportunity, and were thus worth spending over $1 billion to acquire. GSP made their case with various tables and charts, each one demonstrating that the Cubs were all but immune to suffering the consequences of external and internal economic fluctuations. Here’s one showing the sharp increase in franchise values occurring independent of the stock market:

Here’s one showing that, no matter how high ticket prices rise or how much the team sucks, Cubs fans will just keep forking over their money and showing up to games:

One of the more interesting pages in the report sees GSP trying to explain exactly why sports franchise values had begun growing so dramatically, as a way of explaining why it was reasonable to borrow massive sums of money from banks in order to purchase one. Sure, ticket prices increased steadily and broadcast rights got much more expensive, but those factors alone couldn’t explain how the aggregate franchise value doubled from 2000 to 2008. GSP’s way of answering this question was to say that, well, sports franchises are just special:

July 18, 2008

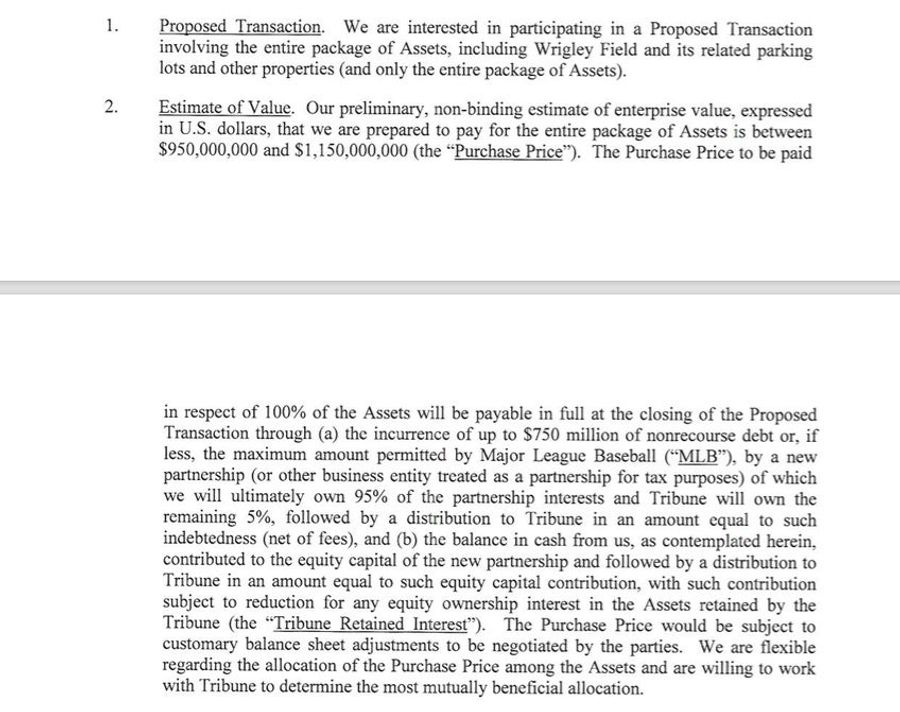

The Ricketts found GSP’s report convincing, and on the day of the deadline for opening bids, they sent their initial purchase proposal to the Tribune. At that point, the Ricketts were willing to pay between $950 million and $1.15 billion for the team:

The bid also made it clear that the Ricketts were happy to go along with the Tribune’s shady tax-dodging scheme:

July 20, 2008

Two days after sending their opening bid, Laura Ricketts, an Obama and Hillary Clinton donor who is the former chairwoman of an LGBTQ Super Pac known as LPAC, sent an email to her father and her brothers Pete (current Republican Governor of Nebraska), Tom (current chairman of the Chicago Cubs), and Todd (current RNC finance chairman), raising for the first time an issue would become an ongoing source of tension within the family: the fact that Tom was enjoying most of the media spotlight.

Hi, Dad and all.

I have scheduled 2 hours for our call this Friday. Also, as I do not have a background in finance, it would be helpful for me to visit with Tom afterward to be sure I fully understand.

Regarding the media coverage, judging from the articles I have seen in the WSJ and Tribune, their reports may mostly be based on who actually signed the bid letters, as opposed to Tom’s request to the Tribune business editor. So, we may still have to watch how we are portrayed in the Tribune at least. Also, their reports now make it seem like it is Tom bidding as an individual as opposed to the family, which is still inaccurate. But, at least for now, we seem to have gotten rid of the Omaha designation.

This is relevant to the issue I raised during our private family conference call on Friday. Now that this process is underway and receiving more media coverage, obviously we are going to have to pay more attention to how we manage the media. We should all be informed and have input on how the media is being managed. The media coverage is also part of the broader issue of the impact the acquisition of the Cubs would have on our lives, particularly those of us living here in Chicago, which we have not yet discussed to date.

Best,

Laura

Tom responded diplomatically:

Hey Laura,

I did flag the new inaccuracy to Dennis and Scott and we will look to clean it up. We got the ‘Omaha’ out but need the ‘family’ in. I don’t know when that will be because we told everyone to that we were not interested in being in any more media. On the other hand, if you prefer a lower profile, this is not the worst outcome.

I don’t believe that the writers saw the bids. We submitted very late in the day for a leak to make the deadline and the articles don’t mention the other people we know to be bidders. I think the Trib thought they were doing what I asked them do and the WSJ implied family money through the “son of” language. Also keep in mind that newspapers always look to use the fewest number of words to make their point.

On other PR fronts away from the Trib and WSJ, I referred four or five other calls directly to Res Publica (Sun Times sportswriter, Reuters, AP, Channel 7). None of these amounted to anything.

After the call yesterday, I decided not have a written statement to send out because the statement would be quoted by everyone and we are trying to avoid any quotes. It is also not clear what the NDA would say about a statement.

I have spoken to writers at Crains, Bloomberg, and will meet the guy covering this at the NYT. The logic of talking to the writers is to tell them that we intend to respect the NDA but want them to be accurate about the family and to have an established dialogue if/when we ever need to talk to them.

Overall, we are being very proactive on the media front and I think we are fairly well positioned. I am happy to give more detailed updates if anything comes up.

On the bigger picture on how it will effect our lives, I agree we should all be thinking about these issues. If anyone has any suggestions on what we should be doing, let’s have a discussion.

Tom

July 23, 2008

The family received word that they would be moving on to the second round of bidding, and that their team would have access to an “electronic data room” in which they would be able to find all the documents they’d need to complete the due diligence portion of the transaction. Tom shared the news via email, and revealed that private equity mogul John Canning Jr., who at one point was seen as the favorite to land the team, had not made it out of the first round:

Everyone,

I spoke to JPM (Grosebuch/Cavatoni) a little bit ago

We are being “invited” into the second round.

Two follow ups:

1. We need to provide them a full list of people that need to have access to the electronic data room.

2. Dates to meet with Tribune folks in August.

They did not tell me how many bidders there were.

They did say we had an “professional” presentation and they said the Tribune Board was very impressed. They mentioned the Trib board several times.

Also, a Tribune reporter called me and told me that Canning was not invited back and their source was reliable. He also said that a Canning source did not deny that but said that they expected things to be “fluid”. So who knows what is next for them. I doubt that it is over for them.

I did, once again, remind the JPM folks that we are interested in a fair process they threw the Fiduciary word out ten times and then we moved on.

That’s all for now. Out with clients and we will touch all the PR bases in the morning.

Tom

July 25, 2008

The family started thinking seriously about how they were going to finance their purchase. The first step in that process was getting yet another presentation from GSP. This was called the “Debt Primer Presentation,” and it explained, in great detail, how and why the family should take on hundreds of millions of dollars of debt in order to buy the team.

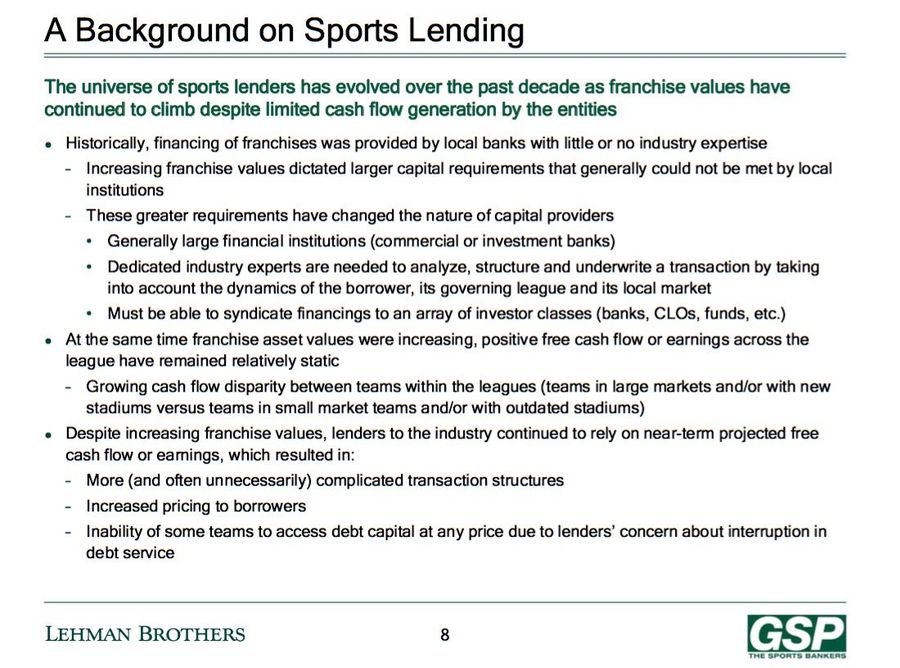

The report starts with a brief history lesson explaining how big banks and lenders got involved in sports acquisitions. This slide explains that as the values of sports franchises grew, so did the need of purchasers to seek financing from brawnier financial institutions. But the big banks were hesitant at first, and for good reason: despite franchise values rising, actual cash flows remained relatively static, ostensibly making it difficult for teams to service their debt:

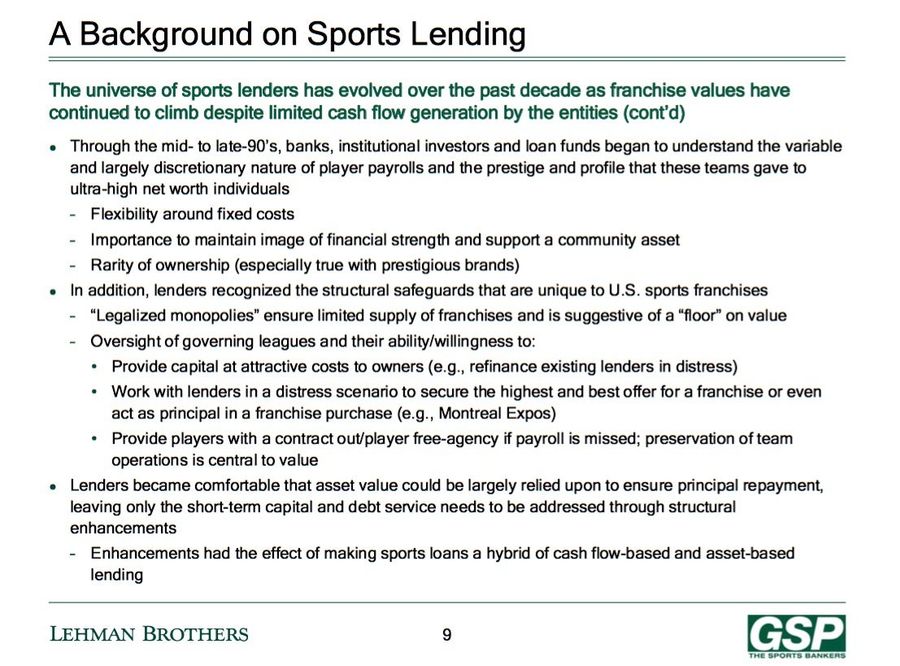

At some point, however, the big banks caught on to something than any longtime sports fan could have told them: Owning a sports franchise, and thus financing the purchase of a sports franchise, is one of the most lucrative scams in America:

It’s clarifying, perhaps, to see that the list of things that makes the ownership and financing of sports franchises so attractive includes so many items that would also be found on a list of things that make being a sports fan such a drag. What this slide describes is the complete insulation of owners from any real consequences. It doesn’t matter if the team is run horribly and no cash is coming in, because they can just cut payroll; the value of a franchise is never going to truly bottom out because leagues are legal monopolies; a bad owner can always just sell his inevitably value-enhanced team for a huge windfall; and even if things get really dicey, the league itself will always be there to provide a bailout, as it did with the Expos—never mind that doing so allowed Jeff Loria to complete his utter destruction of Montreal’s franchise with enough money left over to buy the Florida Marlins and fuck over yet another fanbase. The banks’ conclusion is clear: If even Jeff Loria can run an MLB team into the ground and still come out in the black, why wouldn’t we loan literally any schlub $400 million to buy a team?

This is perhaps a good time to zoom out and consider MLB’s recently frozen free-agent market. There has been no shortage of analysis seeking to explain why baseball experienced a second straight winter in which basically no free agent, whether solid veteran or generational young superstar, had more than one or two teams making competitive offers for their services. There’s no silver explanatory bullet to be found, but things like a poorly negotiated CBA, an increased focus on analytics, more shameless commitments to tanking, and what can charitably be called “soft collusion” all combine to frost the market even while league-wide revenues soar. There’s another factor that should be added to that list, as some wise people have pointed out: the fact that so many baseball teams are swimming in debt.

Ted Lerner purchased the Nationals for $450 million in 2006, and the “Debt Primer Presentation” GSP sent to the Ricketts includes the details of that sale as a case study for how a highly leveraged purchase can work. Lerner took on the maximum amount of debt—$360 million—in order to purchase the team. Jim Crane bought the Houston Astros for $615 million in 2011, reportedly by taking on $300 million in debt; the Dodgers ownership group assumed $412 million in debt when they purchased the team in 2012; the new Marlins owners needed $300 million in financing from JPMorgan in order to purchase the team in 2018. And these are just the financing numbers that have been publicly reported.

This is not to say that these leveraged teams don’t have enough cash to service their debts and be active in the free-agent market, but it does provide them with yet another excuse not to. You don’t even need hard collusion to whittle Bryce Harper and Manny Machado’s prospects down to one or two offers, just enough excuses in the pot—analytics, the luxury tax, the success of tanking teams, Albert Pujols—that any owner, at any time, can grab onto in order to convince himself that he can’t spend any more money on player payroll. The very structure of how these teams are purchased conveniently gives owners a pretty good built-in excuse.

The “Debt Primer Presentation” gives us a more detailed look at how the Ricketts were starting to make plans for financing their purchase:

The plan laid out in this slide, based on conversations with JPMorgan, would have the Ricketts taking on $750 million in debt in order to pay a $1.13 billion purchase price. One thing to note is that this plan would shift the majority of the debt from the team itself to a holding company, thus allowing the Ricketts a much better shot at satisfying MLB’s debt service rules. This is a technique that other teams have used in order to skirt MLB’s debt rules.

In the following days, the Ricketts’ efforts to acquire the Cubs kicked into full gear. Emails in Joe’s inbox indicate that Tom Ricketts and Alfred Levitt, the president and general counsel of TD Ameritrade’s holding company, were hard at work with GSP to create a financial model for the franchise, that an architectural firm was hired to analyze Wrigley Field as part of the due diligence process, and that Deloitte was hired to provide audit and tax review services. The family also retained former Arizona Diamondbacks president Rich Dozer to serve as a consultant.

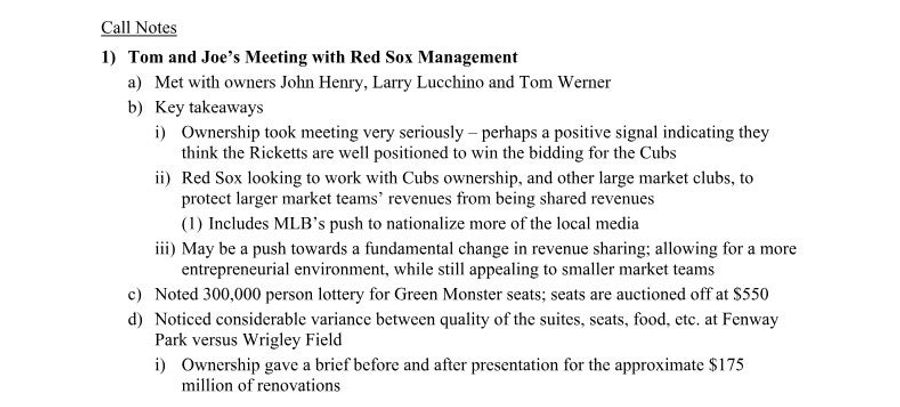

September 5, 2008

The Project North Side team held another conference call, the notes from which were circulated afterwards. A portion of the call was dedicated to recapping a meeting that Tom and Joe Ricketts had with Boston Red Sox management, in which they apparently discussed how much money can be made off stadium renovations and how they might team up to make MLB more hospitable to super-rich teams:

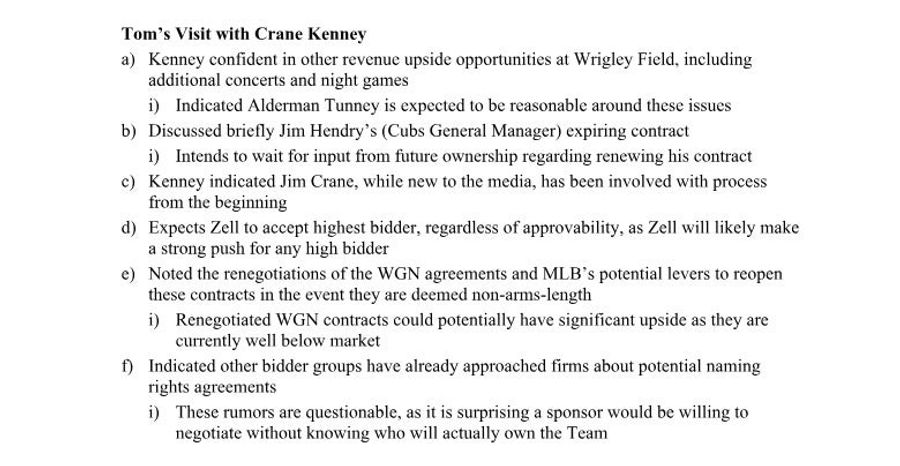

The call also recapped a conversation Tom had with Crane Kenney, then the Cubs’ president of business operations, in which they discussed the possibility of renegotiating the team’s broadcast deal with WGN (which was then owned by the Tribune Media), holding more concerts and events at the stadium, and Zell’s interest in going with the highest bidder:

September 6, 2008

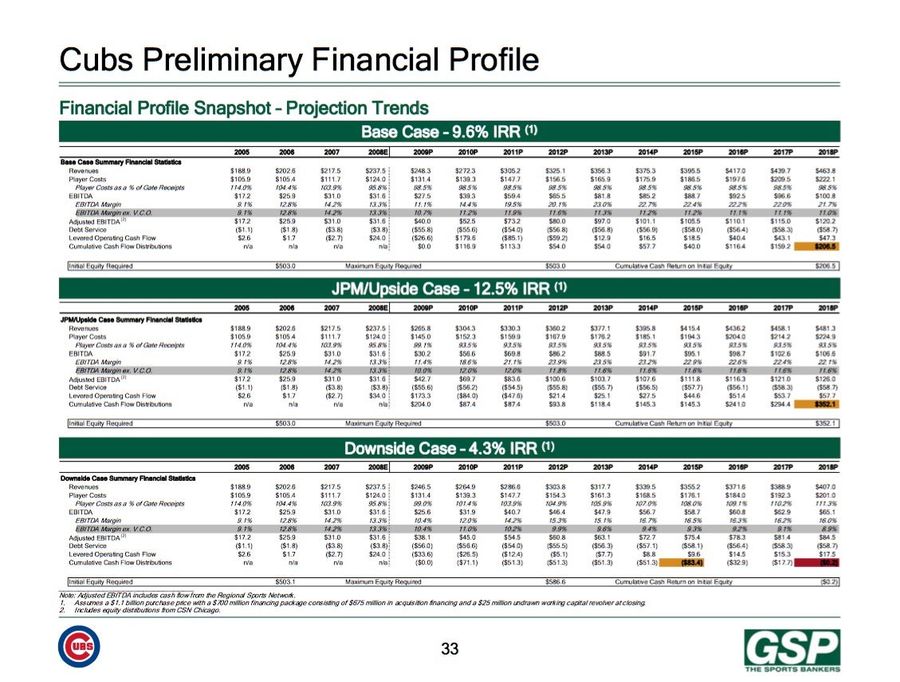

The family received a benchmarking analysis from GSP, which used information about the Cubs obtained from the secure data room, along with various financial assumptions, to paint a picture of the team’s current and projected finances. The analysis presented three projections: a base case, an upside case, and a downside case.

Even the downside case, which is the most pessimistic projection, still comes with a 4.3 percent internal rate of return (IRR), a metric that estimates the profitability of an investment. (High IRR is good, low IRR is bad.) All three of these cases also assume a $1.1 billion purchase price and $700 million in financing; the actual price tag for the team ended up being $845 million, which required just $450 million in financing. Each case also projected a steady increase in player costs, but the Cubs’ player payroll actually took a few dips in the years after the Ricketts took over the team. The upside and base cases also project the team to have a solid chunk of levered operating cash flow—the amount of cash a company has left over after meeting all of its financial obligations—by 2018.

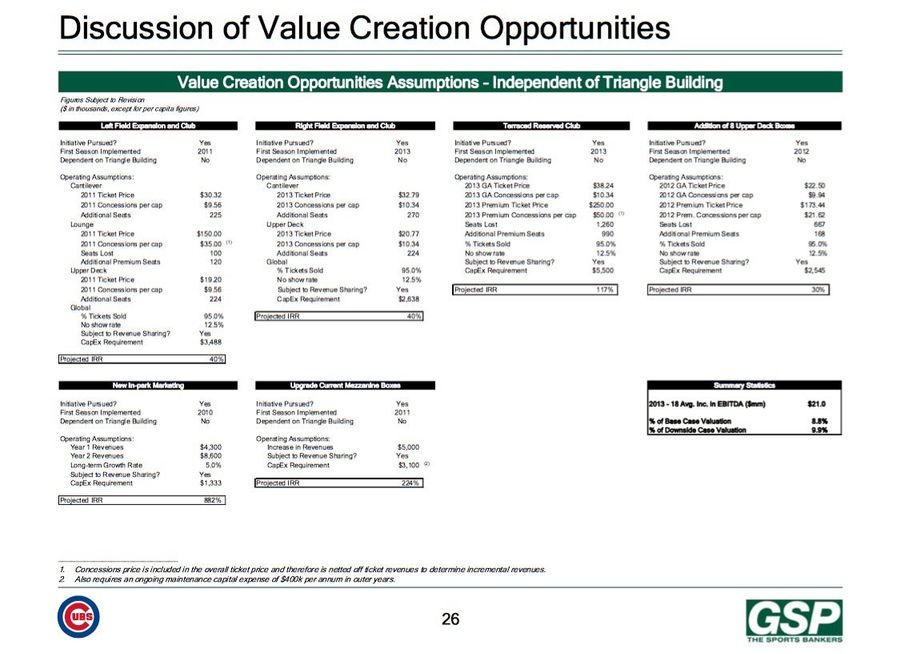

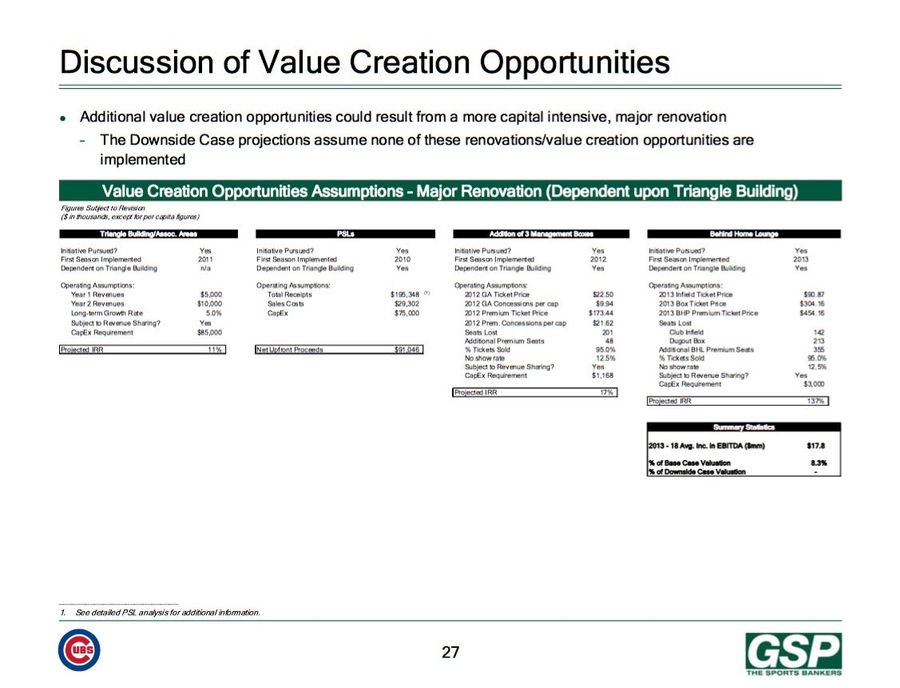

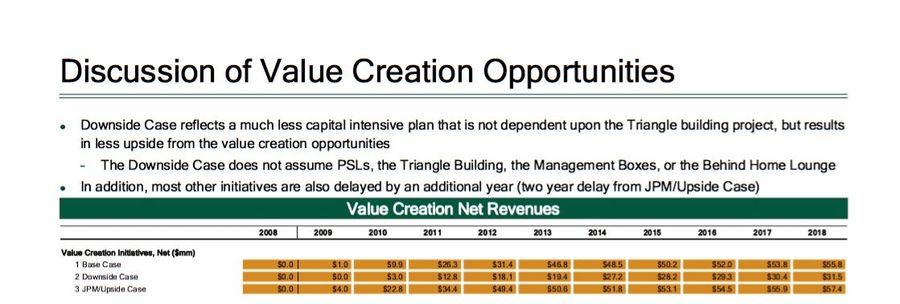

It’s not surprising to see that the Cubs, a storied franchise with consistently great attendance and a dedicated fanbase, profiled as a good investment, but the analysis also assumed that the Ricketts would pursue certain value-creation opportunities, such as stadium renovations and instituting a PSL program, a practice popularized by NFL teams which requires fans to pay a fee just for the opportunity to purchase season tickets. The analysis in the base case attributed 8-9 percent of the total overall value of the team to potential net revenue produced by these opportunities. The analysis suggested specific stadium renovations that could be taken on, each of which came with a strong projected IRR:

This table shows projected annual net revenues produced by these improvements rising above $50 million in both the base case and upside case.

It’s hard to say if the team ultimately reached these particular benchmarks; they have yet to get around to creating a PSL program, but continue substantial renovations at Wrigley Field that began in 2014. What these numbers do show, though, is that the ongoing stadium renovations were a core part of the Ricketts’ business plan even before they purchased the team. They are also yet another example of how the consequences of MLB’s exploding franchise values trickle down to the fans. If some rich people want to spend a bunch of money they don’t have on a baseball team, they’re going to have to subsidize their decision with some new revenue streams. Sometimes that means creating PSLs or raising ticket prices or slashing payroll, sometimes it means turning a once-charming stadium into a place where rich people can pay a premium price to sit in a padded seat and enjoy the carving station in a charmless room bearing a name like the Bud Light Cold Hard Hardball Club.

September 15, 2008

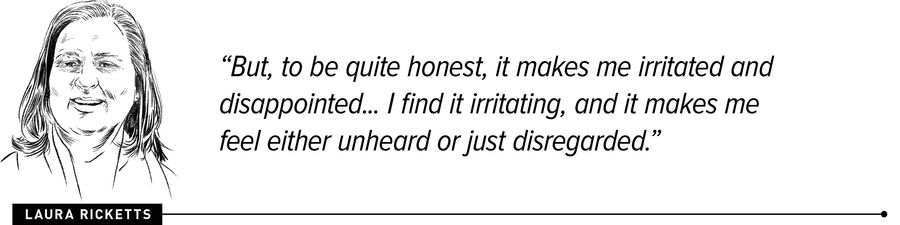

The issue of Tom being portrayed as the face of the family came up again, with Laura sending an agitated email to the family pointing out that Tom was the subject of a flattering article in Crain’s Chicago Business:

Tom,

This Crain’s article is a positive and very flattering piece about you. But, to be quite honest, it makes me irritated and disappointed, particularly in light of the discussion we had during our family conference call last Monday. I realize that we cannot control the media. But in this instance you provided input at least in as far as you steered the reporter in a certain direction. I find it irritating, and it makes me feel either unheard or just disregarded.

I suggest that we, as a family, talk further about this and the media generally. What is the schedule and agenda for tomorrow’s meetings? Will we have time for the five of us to have a private meeting aside from all the lawyers and bankers?

Laura

Joe chimed in a few hours later in support of his daughter:

Laura,

I’m really pleased that you express your thoughts and feelings freely. I’ve been thinking for a while that feelings such as you express may be prevalent among the other family members but were just kept suppressed. The thought was a quandary for me. This is a family enterprise and activity and so anything that would not pull the family together should be avoided and/or eliminated. This is why I suggested that WE put out a Press Release indicating that this effort is a family effort and that we designated Tom as project leader. However, it appeared to me that you folks didn’t seem to positive toward the approach so I let Tom continue to take the lead.

There isn’t any doubt in my mind that if any of us are irritated, feel unheard or disregarded then we should not buy the Cubs. We should take some time to be by ourselves tomorrow as we need top make this effort a positive and not a negative event.

J. Joe Ricketts

Tom then responded, perhaps a little defensively:

We certainly can discuss this tomorrow. I am open to any suggestions on how to engage with the media. I would suggest we include Dennis so that none of you think I ignored the suggestions from the last family call on the topic.

In the end, every single bidder in this process represents a group and the media are going to focus on the lead person in the group. I am not sure what can be done about that.

Overall, I think we have handled the media extremely well. We have avoided receiving media attention and what little media we have received has been positive, if not evenly distributed. We are not now and have never asked a reporter to write a story on us (or me) and I don’t think that we should change our policy. We have received high marks from the league for this strategy. In the end, the only people that matter right now are at MLB and they know it is a family bid.

Laura got the last word, though:

Tom,

I appreciate your point about MLB’s perception of us, but I would argue that, in the end, the only people that matter are our family members. This is not just an issue of what we need to do to impress the MLB, but also what we need to do to be respectful to everyone in the family. Also, I think this media issue is actually part of a bigger issue that deals more with our family dynamic. As such, I suggest that we have a discussion with just the family. If you’d like we could include Dennis for part of that discussion but I don’t really think he will provide any insight in to what is at the core of this issue.

September 16-17, 2008

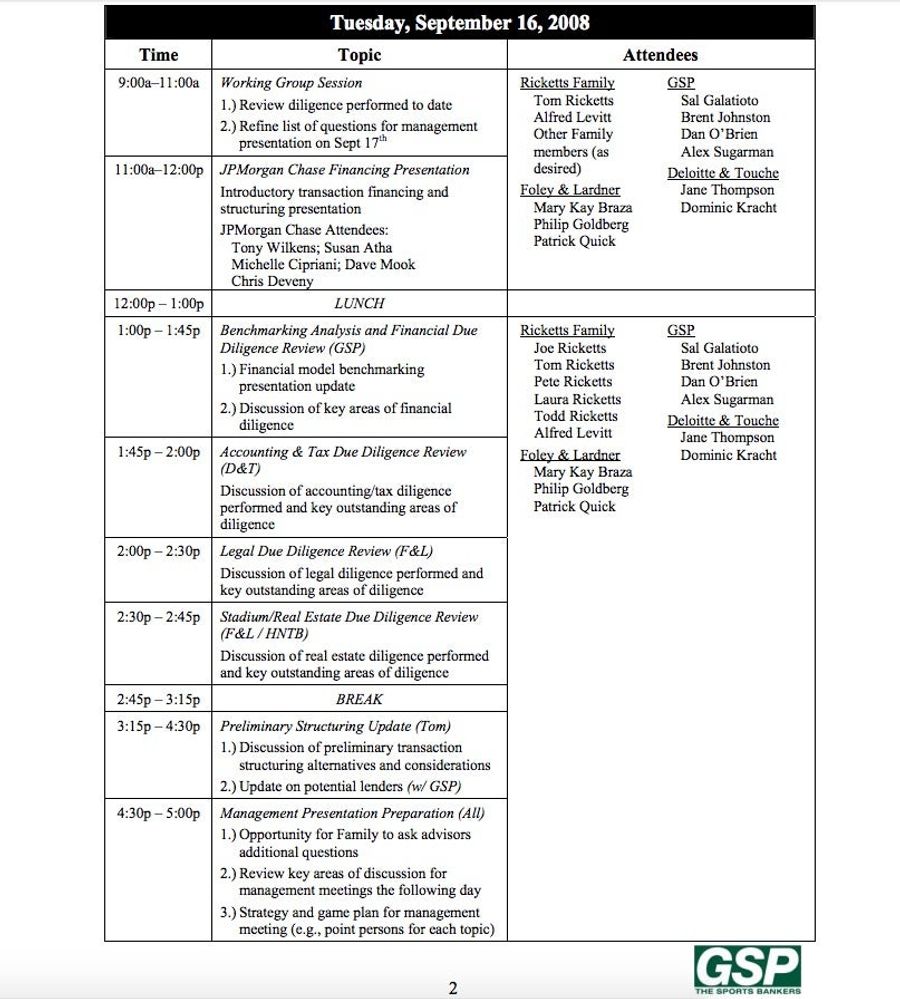

The Ricketts and other members of Project North Side flew to Chicago to have a few important meetings with representatives from the Cubs and the Tribune so that the Ricketts could gather as much information as they could about the Cubs’ financial situation and the two sides could dive more heavily into the due diligence process. The trip consisted of two full days of meetings attended by an army of lawyers and consultants. The day before the trip, a 46-page agenda was sent around to attendees.

The first day consisted of multiple meetings attended by only members of Project North Side, the purpose of which seemed to be updates about where they were in the sale process and figuring out what information they still needed from the Cubs and Tribune at the next day’s meeting:

The next day saw the Project North Side team at one long meeting with Cubs and Tribune executives at Wrigley Field. The agenda for that day’s session listed 15 topics of conversation covering everything from the importance of the Cubs’ stake in CSN Chicago (the agenda says that stake represented 15-20 percent of the team’s total value) to revenue sharing and the structure of a potential deal.

September 18, 2008

Following the meetings in Chicago, Levitt sent an email to Joe Ricketts giving him a rundown of the action items that had come out of the meetings. Most are banal, but one raises the possibility of doing some digging into a rival bidder:

2. We discussed updating our competitive intelligence and digging deeper into Utay and the other potential bidding groups. How do people propose we advance this lane of work? With respect to Utay, can Lee Einbinder give us more insight anything beyond what he has?

Levitt is referencing Marc Utay, who is currently the managing partner at Clarion Capitol and who at the time had interest in buying the Cubs. Levitt seems to be suggesting that Joe talk to Lee Einbinder, then a banker at Lehman Brothers, to try to pump him for information about Utay. The next day, Levitt and Joe had a brief email exchange in which they, apparently based on a conversation with Einbinder, decided that Utay wasn’t much of a threat.

From: Alfred LevittSent: Friday, September 19, 2008 11:40 AMTo: Joe RickettsSubject: Re: Action Items/Follow-up

Without becoming complacent about Utay, Lee’s comments today gave me some comfort that Utay might not be loaded for bear.

Joe Ricketts

Sep 19, 2008, 3:58 PM

I agree

September 23, 2008

The Ricketts family began to discuss how they might begin exerting some control over the media coverage of their bid for the Cubs. Previous correspondence between the family remembers reveals that they were annoyed at being portrayed as a bidding group from Omaha rather than a group with strong ties to Chicago.

The family got word that the Chicago Tribune was working on a feature about their pursuit of the Cubs, and so the VP of Res Publica, the family’s PR firm, sent around an email outlining potential talking points that surrogates of the family could feed the paper:

Dear Ricketts,

Attached and below are possible talking points for some messages for any friends and associates who speak on your behalf about your effort to buy theCubs. I think these messages would resonate well and help communicate that:

1. This is a family bid.

2. That the family has deep ties to Chicago and respect for baseball.

3. That the family’s focus will be on delivering excellence for Cub fans.

You can alter as you see fit. It appears the Tribune is moving fast with their feature piece and have already started reaching out to people on their own.

Ricketts Family Cubs Bid— Possible Surrogate Talking Points

* The Ricketts family has deep ties to Chicago, all four of the siblings attended college here and Tom, Laura and Todd have called Chicago their home for many years.

* Baseball and the Chicago Cubs have been a source of Ricketts family bonding over the years. They have attended more Cubs games than they can count. As a result, they have great respect for the game of baseball and for this great franchise.

* The family intends to own this team for generations to come. They will be focused on Cub fans and on enhancing their experience at the games. Most importantly, they will be committed to building a consistent championship tradition. Being goal-oriented, success-driven and customer-focused is a family culture that was created by Joe and his wife Marlene founding Ameritrade and that is carried on today by their children.

* This family has the expertise to develop and execute a comprehensive plan for success. Tom as the point person for the family’s bid will, if they are successful in acquiring the team, have the talents of his whole family to help lead the way to achieving their goals. The family board of directors will be able to boast of a self-made billionaire, three successful entrepreneurs and a corporate lawyer. All of them will be focused on making a great baseball franchise even stronger.

Pete and Joe both replied to the email affirmatively, but Laura was unable to hide her disdain for the last bullet point, which suggested highlighting Tom’s role as a point person:

This looks fine to me. But I would not share the very last point. That one seems really odd to me.

My time has been very tight since yesterday’s conference call. I have not yet had a chance to get in touch with the people I would recommend to the Tribune. I will get those names to you tomorrow.

Best,

Laura

September 28, 2008

Joe Ricketts received an email from a friend seeing if he like to come over to watch a Nebraska football game. When he responded to say that he couldn’t come, he blew off some steam about how arduous the Cubs’ sale process had been:

Thanks for the invite. I just opened this email and it is to late.

Tom and his two girls were here this week end so I watched the game with him. Think we’ve got the start of a good program at NE. I like BO.

Cubs – we still are working hard under the direction of Tom but myself and four kids are all involved. We think there are really only two bidders, ourselves and Cubin. Really can’t get any info on the other reported bidding groups. The price is high and the financing markets are bad so I’m not sure they really exist at the moment. We have to give our final bid in the next couple of weeks and are ready to do so with a little more information on what is offered for sale. This is the most complex deal I’ve ever been involved with and we have the best consultants I’ve ever worked with. All in all we have over 30 consultants working on this evaluation and helping to put together the bid. There are many different aspects and angles that have to be considered in order to come up with a bid that would be proper for us and the seller. Many different skills and talents are needed for the evaluation. The seller says they want this done by the end of the year so we’ll see; the seller is really the one going slow.

October 2, 2008

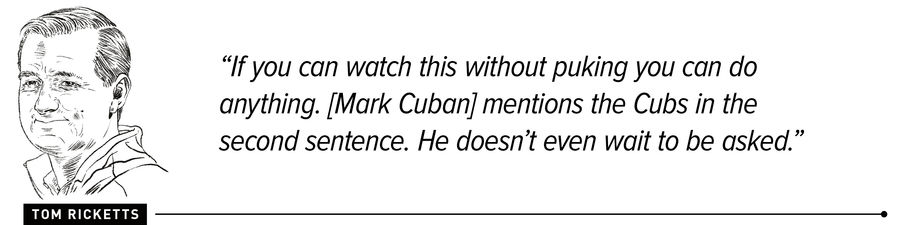

Tom sent an email to the family with a link to a Fox Business interview with Dallas Mavericks owner Mark Cuban, who at the time was the Ricketts’ biggest competition for the Cubs. Tom was not pleased by the interview:

If you can watch this without puking you can do anything. He mentions the Cubs in the second sentence. He doesn’t even wait to be asked.

Tom

Laura responded:

Yeesh!

Looks like he’ll be at the game tonight.

Zell was at the game last night. I wonder if Cuban will be sitting next to him tonight.

Laura

November 24, 2008

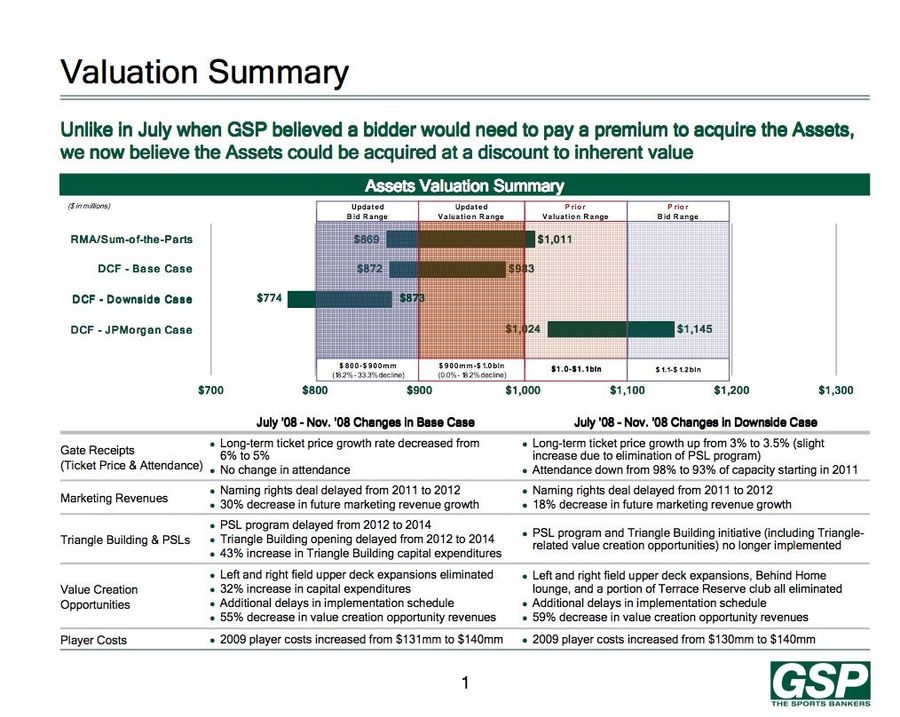

After having received word from the Tribune that November 26 would be the deadline for the second round of bids, GSP sent the Ricketts an adjusted bid proposal in which they argued that the Cubs could actually be acquired for a discount from the inherent value of the franchise based on factors including a decrease in ticket price growth projections and a delay in a naming rights deal and various stadium renovations. GSP updated their base and downside cases to include more pessimistic projections, and came to the conclusion that the team could be had for a bid in the range of $800 million:

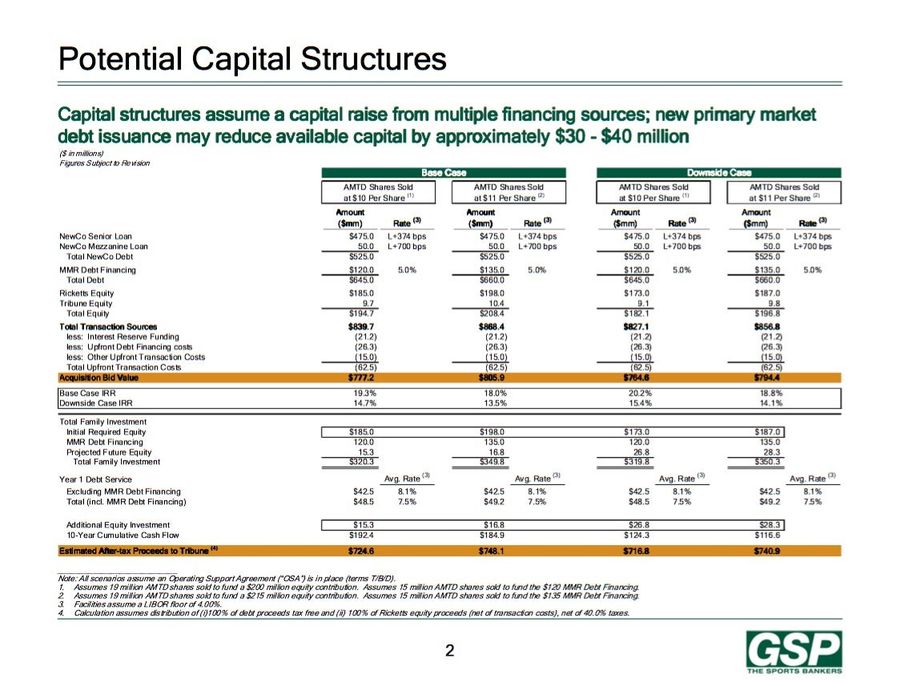

GSP also put together more specific projections for the deal’s capital structure, which would involve the Ricketts borrowing around $650 million and contributing around $200 million of equity raised from selling shares in TD Ameritrade, which were owned by the family’s Education Trust:

This proposed structure greatly increased GSP’s projected internal rate of return in both the base and downside cases.

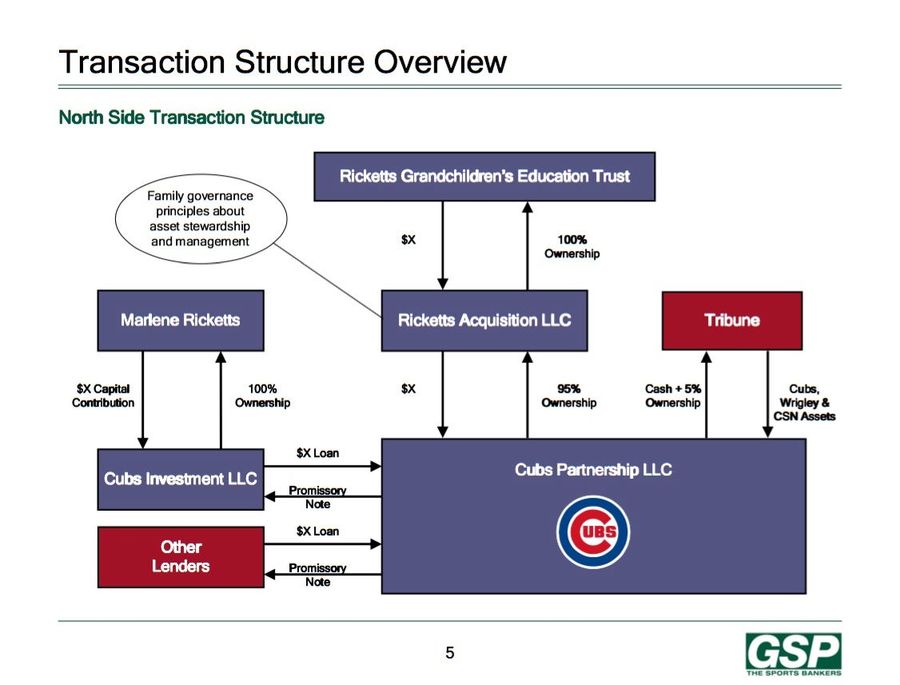

GSP also provided a helpful graphic laying out the proposed structure of the leveraged partnership, which now included an additional “loan” coming from Joe Ricketts’s wife, Marlene, funneled through yet another LLC:

Tom Ricketts recently claimed that his father is “not involved with the operation of the Chicago Cubs in any way,” in an effort to distance himself and the team from racist emails that Splinter found in Joe’s inbox. Perhaps it’s true that Joe is not involved with the Cubs on a daily decision-making level, but the transaction structure laid out in the above slides show that he is unequivocally a co-owner of the team. The money coming from the Education Trust—which accounts for all of the equity put into the sale—and from Marlene Ricketts came first from selling off shares in TD Ameritrade, the company Joe founded. That’s his money, through and through, and thus there is no extracting the Chicago Cubs from Joe’s orbit.

Through the same spokesman, the Ricketts family sent this statement in response to questions about Joe Ricketts bankrolling the purchase of the Cubs and his involvement with the team:

The Ricketts family purchase of the Chicago Cubs in October of 2009 was well documented. It is well known that the wealth created by Joe and Marlene Ricketts by building Ameritrade would provide the funding for the trust, controlled by their children, to buy the Chicago Cubs.

November 26, 2008

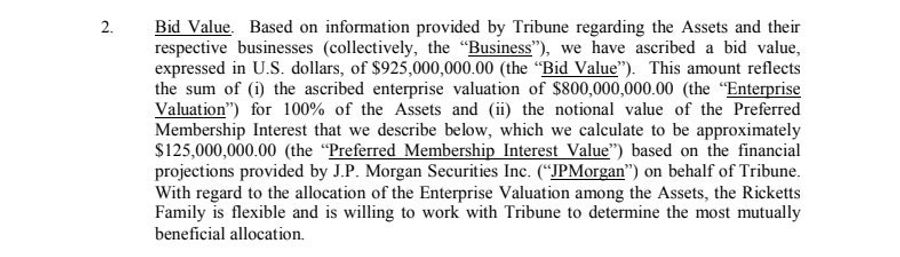

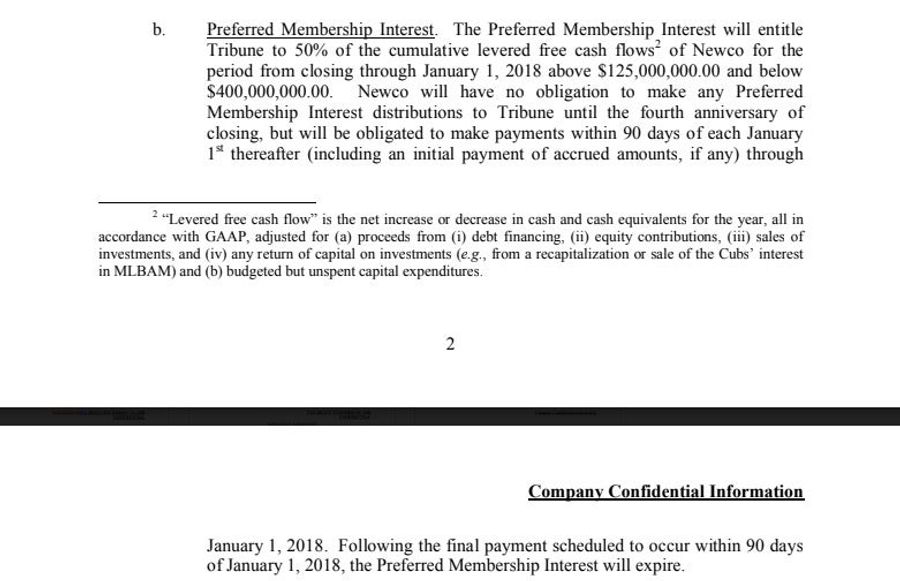

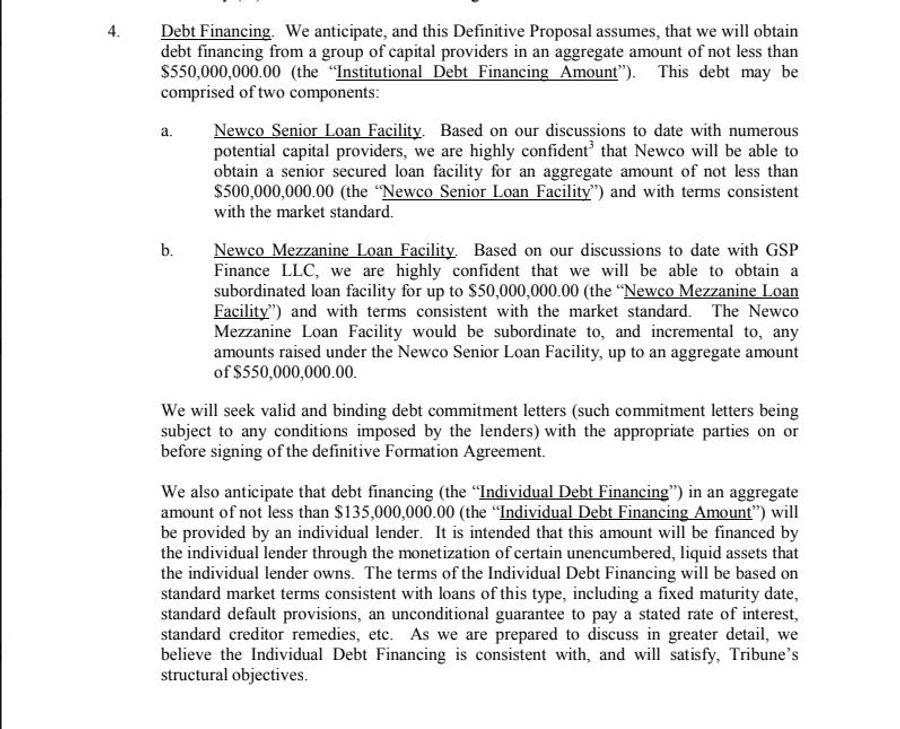

The Ricketts heeded GSP’s advice, submitting a definitive bid proposal to the Tribune in which they ascribed an $800 million value to the Cubs franchise and its associated assets. This proposal came with a complicated wrinkle, though, which the Ricketts claimed could raise the final price tag to $925 million.

The Ricketts proposed paying $786,250,000 for a 95 percent stake in the Cubs upfront, and granting the Tribune preferred membership interest in the new LLC the Ricketts and Tribune would be creating in their leveraged partnership. This preferred interest membership would provide the Tribune with annual cash payouts, contingent on certain factors, that could reach a total value of approximately $125 million.

The proposal also detailed the Ricketts’ debt financing plan. The “individual lender” mentioned in the last paragraph below is almost certainly Marlene Ricketts, who at that point was being relied on to provide a $135 million loan:

December 7, 2008

The Tribune company filed for bankruptcy protection.

January 2, 2009

Levitt sent Joe a Wall Street Journal full of handwringing about how owning a major sports franchise may no longer be a lucrative venture, citing the Tribune’s bankruptcy, the New York Times selling its stake in the Red Sox, and the financial woes of the Wilpon family, which owns the New York Mets, as evidence. Levitt wanted to assure Joe that such developments hadn’t scared lenders away from the Cubs deal in an effort to urge caution about any attempts to increase their bid—which was lower than two other remaining bidders—and to float an idea about how they might be able to squeeze more money out of the Tribune by renegotiating the Cubs’ deal with WGN:

The WSJ article below was among those circulated in the Cubs daily clips. We have pressed the bankers on the question of whether the NYT’s sale of its interest in the Red Sox, the Wilpon family’s rumored (and disputed) sale of the Mets, and other potential teams being sold as a result of the financial meltdown, would cause us to revisit the analysis that undergirds the family’s $800MM bid. To date, and not surprisingly, the bankers are standing firm.

As long as we bid at a level where projected (conservative) revenues will comfortably support debt servicing, I think we are fine, but we will need to consider with great care any decision to increase our bid that costs real money. We may be able to improve the economics of the family’s bid by demanding additional concessions in the media contracts; a tactic that was not feasible prior to the Tribune’s bankruptcy filing. If we can obtain improved terms on the WGN contracts, for example, we can provide more cash at close without requiring the family to come out of pocket with incremental dollars. Cash at close will be King for the creditors and, thus, we are acutely focused on exploring this option.

Joe didn’t seem to be too worried about the family’s bid, but did ask for more explanation of the WGN angle:

Thanks Alfred,

Tom told me that he started working on this a couple of days ago and with the help of you and the rest of the team I feel comfortable that a solution will be formulated that will improve our position. It is my impression at the current time that we are in the best position relative to everything except to price. As we know, both of the other two bidders submitted a higher price but the other aspects of their bid/position may not be attractive as ours. As we all know, if we narrow the dollars in the bid we’ll be in a better position to win what we want.

I do not understand the second sentence in your second paragraph. Please explain how the bankruptcy changes our consideration of the media contracts.

Anxious to see what you all come up with on the WGN contracts.

Levitt explained:

While the potential to renegotiate the media contracts existed before the Tribune bankruptcy filing – indeed, our initial bid was contingent on obtaining $5MM in concessions on the WGN contracts – the bankruptcy has put squarely into focus the need to maximize cash at close in order to satisfy the creditors whose support is critical. We are, therefore, exploring ways to squeeze more concessions out of the WGN media (TV and radio) contracts that provide for an additional $6MM in value above the $5MM we had originally anticipated – i.e., $11MM annually. The most obvious way to do this is to increase the broadcast fees WGN pays the Cubs, require that WGN pays the Super Station fee (~$3MM annually), or some combination of these. Tom is also exploring the potential value to the Cubs if the team were able to terminate early the WGN contract, permitting the team to develop more efficient ways to monetize its content – e.g., its own broadcast channel? If we can get our arms around the potential value inherent in an early termination of the contracts, this option may be the most interesting. My choice of the word “feasible” below was too strong; these options existed to some extent before the bankruptcy but the bankruptcy provides the potential club that puts in play more options.

January 6, 2009

Levitt provided more suggestions for how the Ricketts could improve their bid, and floated the idea of tapping into yet another one of the family’s trust funds, which had $28 million in it:

With the Reserve Yield Plus having made its initial distribution, the 1994 Dynasty Trust has around $28 million in cash. If the family decided to increase its bid for the Cubs, the cash in that trust could provide the source of funds rather than an incremental sale of shares by Marlene providing the additional money.

I would guess that, as between (a) Marlene selling more shares and (b) using cash in the Dynasty Trust, you would prefer for Marlene to sell given your other strategies for the assets in trust - e.g., the family bank - but I want to confirm that I was correctly anticipating your thinking.

Joe made it clear that the Dynasty Trust was off limits:

The Dynasty Trust assets are not available for the Cubs. I’ve said this from the beginning and haven’t changed my mind. thx

January 6, 2009

Mark Cuban officially dropped out of the bidding war. He explained his decision in a lengthy post on his personal blog, citing the team’s astronomically high valuation and the declining credit market.

January 9, 2009

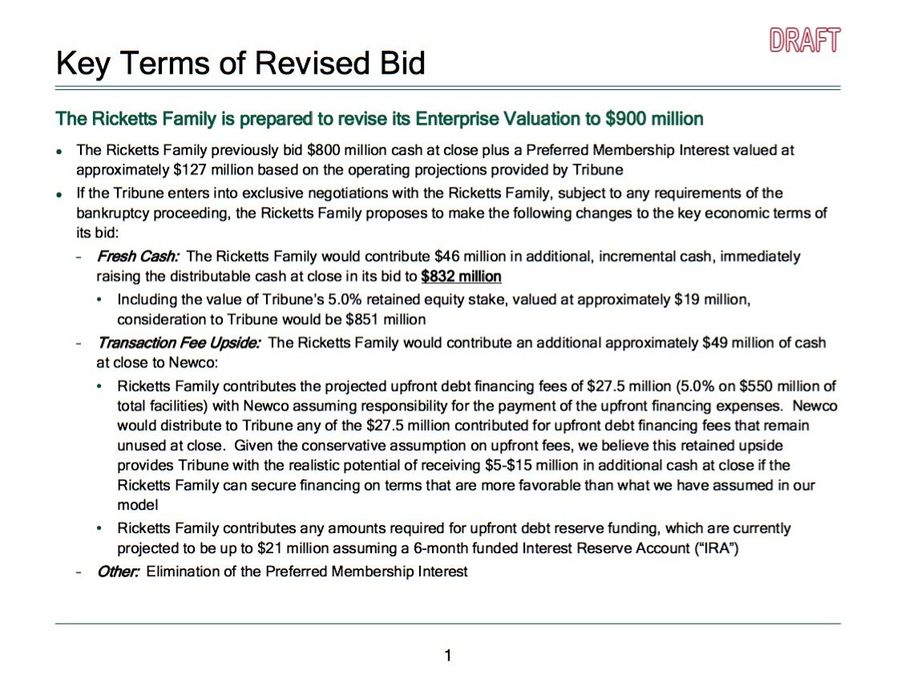

The Ricketts decided to make a revised bid to try and increase their chances at securing the Cubs. GSP prepared a three-page document outlining the family’s new bid.

The Ricketts decided to do away with the preferred membership interest component and replace it with more cash upfront. This new bid would bring the full value of the Cubs to $851 million, and would have the Ricketts contribute an additional $27.5 million in upfront debt financing expenses.

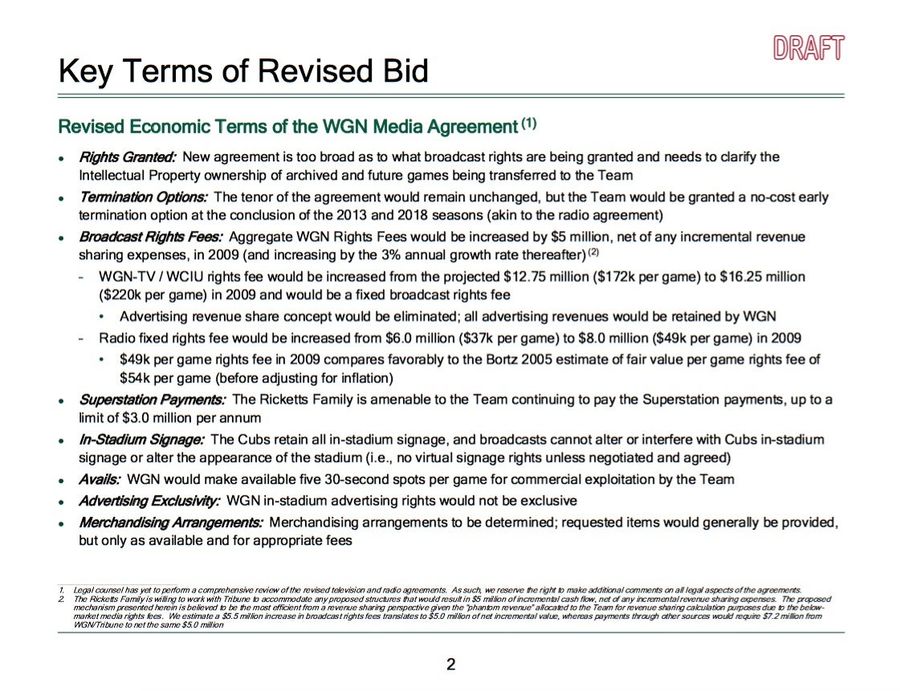

The new proposal wasn’t just about ceding more money to the Tribune, though. The Ricketts also went ahead with Levitt’s plan to squeeze more money out of the Tribune through a renegotiated broadcast deal between the Cubs and WGN that would include higher rights fees and free advertising spots:

January 16, 2009

Tom reached out to Nils Larsen, a Tribune exec working on the sale, to get an update on the company’s decision-making timeline. Nils sent back a somewhat ominous response, which Tom forwarded to the rest of the family, referencing “greater movement” from other bidders:

Tom:

We have a board meeting early next week at which we will present the various offers and a recommendation as to how to proceed. After that we will inform the various constituents in the bankruptcy of our decision and inform the bidding parties. I would expect bidders to know by the middle of next week.

There was considerably greater movement from some bidders than I anticipated which required more analysis and has accounted for the delay.

I am happy to discuss further if you would like.

Nils

Laura seemed slightly concerned in her reply:

Thanks, Tom.

Can everyone please address email to my [redacted] account.

I am traveling now until Jan 24th, and all my Yahoo email goes directly to my iPhone. So, I will get emails much faster at that account. Thanks.

What do you make of the “considerably greater movement from some bidders” comment? Also, have you had any correspondence with Nils other than this email, or received intelligence from any other sources.

Best,

Laura

January 22, 2009

Six days later, all worries were put to rest. Tom emailed the rest of the family to let them know that their bid had been selected, which meant that the family could move into an exclusive negotiating period with the Tribune:

Everyone, just got off with Nils. We did get the nod in this round. The thought is to send out this statement tomorrow morning. Next steps is a meeting with all of the advisors toward the end of next week.

Alfred- will you forward to everyone on the deal team. Thanks. Tom

January 23, 2009

Laura’s issues with Tom getting all the publicity finally came to a head. She sent an email to the family expressing her annoyance:

FYI, ESPN TV just did a whole segment on Tom buying the Cubs. They even interviewed a Tribune reporter who also referred to Tom as the purchaser.

Joe responded almost immediately, but only to Laura:

Tell the PR to get the press straight

Perhaps realizing that he had meant to send the previous message to Tom and the rest of the family, he sent another email to the whole group:

Can PR get the press straight. Maybe we should give consideration to finding a new PR firm

Pete tried to calm things down:

Folks,

I appreciate the concern to make sure the PR stays on message but I would also like to remind you that, based upon my experience for 14 months during my campaign and all my time at AMTD , the press says any damn thing they feel like if it will get them audience.

Pete

Laura suggested that the family instruct their surrogates to stop talking to the press:

Do you think someone should ask Larry and Curt and any others not to speak to the media?

Tom clarified that the latest round of media coverage did not come from his surrogate:

I spoke with Larry this morning and he said a reporter contacted him through facebook asking for a quote but he declined.

Laura started to get even more annoyed:

OMG. Just saw Tribune front page at the Newseum in DC. The heading is “Meet the Cubs’ $900 Million Man” with a big photo of Tom next to it. Which is disappointing.

I definitely think we should request that various friends, specifically Larry and Curt, not speak to the press for now.

January 27, 2009

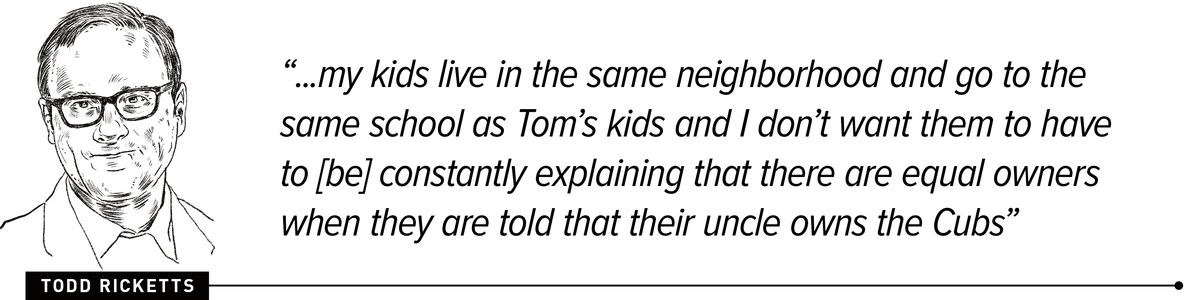

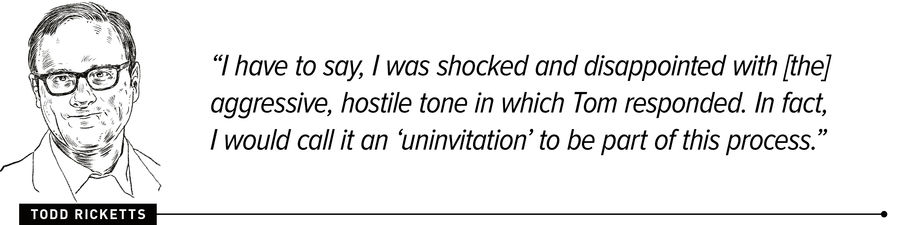

The fight over press coverage resumed when Todd sent an email to Joe and Pete recapping a conference call the rest of the family had taken part in. The call went poorly, and left Todd thinking that maybe buying the Cubs wasn’t such a great idea after all:

Dad and Pete,

We missed you at this morning’s call and I think it would have been helpful if you had been there.

Tom updated us on the current discussions on the finance side which he can give to you later, but more importantly we had a discussion about the PR and media.

Laura and I, again, expressed our concern about the public perception on the deal. I expressed my thought that it is crucially important that we try to keep the press clear on what the new ownership of the Cubs will look like. My reasoning for this is that my kids live in the same neighborhood and go to the same school as Tom’s kids and I don’t want them to have to constantly explaining that there are equal owners when they are told that their uncle owns the Cubs. The reason I am sensitive to this is that even today I feel as though my input and ideas are disregarded among our family just as they were when we were kids. This is not the feeling I ever want my kids to have and because they are the beneficiaries of the education trust that is proposed to finance the deal I take it very seriously.

To that end, I suggested that Laura and I start working more closely with Res Publica on formulating our PR and also suggested that this may be a good way for others of us to start becoming more involved in the process while at the same time alleviating some of the many tasks Tom is trying to address at the moment.

I have to say, I was shocked and disappointed with aggressive, hostile tone in which Tom responded. In fact, I would call it an “uninvitation” to be part of this process.

I guess what really became clear to me is that this deal is not about having a shared asset that we can work together or something that will bring our kids closer together. And because of that I am more skeptical than ever as to whether this is a good idea for our family and/or a good use of trust investment dollars.

Sincerely,

Todd M. Ricketts

It’s hard to say where the conversation went from there. Whatever offline discussions between the family may have occurred did lead to one conclusion, though: The family needed a new public relations firm. A few days later Joe sent an email to Levitt saying that he was “not satisfied with Res Publica” and would like to find a new PR firm once the deal for the Cubs was closed.

In response to questions about intra-family tension during the sale process, the Ricketts family sent the following statement through a spokesman:

Any family discussion in ten-year old emails of media coverage would be a natural thing to discuss as the siblings were being thrust into the public arena for the first time in their lives. The siblings are extremely close and proud of their accomplishments together. They are looking forward to winning another championship in 2019 and continuing their commitment to the city of Chicago and Cubs fans.

February 17, 2009

The Ricketts family had to start filling their coffers with the necessary cash to fund their purchase of the Cubs. Levitt sent an email to Joe letting him know that they were about to go through with the planned sale of the TD Ameritrade shares owned by Marlene and the family’s Education Trust:

Joe –

So you have the numbers of where we landed:

* Marlene sells 15mm shares @ $11.85 for gross proceeds of $177,750,000. Sale proceeds net of taxes and fees is $149,310,000.00.

* Education Trust sells 19mm shares @ $11.85 for gross proceeds of $ $225,244,800. Sale proceeds net of taxes and fees is $189,205,632.

* Total net proceeds from the sale are $338,515,632.

* We will move Marlene’s cash into her account at UBS and the trust’s cash to Bessemer.

Levitt followed up to make it clear that the Ricketts now had plenty of cash to fund the equity portion of the Cubs sale:

I should have mentioned the most important takeaway: these proceeds, when combined with the proceeds realized from the sale of the S&P 500 SPYDERS, means we have all the cash we need for the equity element of the Cubs purchase. As it stands, the family now has $387mm in cash firepower for the Cubs deal, which is going to be an important strength for us as we work with the Tribune’s creditors and bankruptcy court.

February 18, 2009

The Ricketts planned a family meeting to discuss their long-term financial planning, and the agenda for the meeting carved out an hour-long block for them to discuss “Cubs Media Issues” with Lee Hausner, whose business is advising wealthy families on how to stay wealthy and better communicate with each other. After looking over the agenda, Laura, apparently still smarting over the PR issues, asked Joe if more of the meeting could be dedicated to talking about the intra-family tension over the Cubs sale:

Hi, Dad.

I was just looking over the draft agenda for the family meeting next week and was thinking that, given what has transpired personally among the four of us siblings lately (regarding the Cubs stuff), it would be really helpful to have more time talking through family dynamic issues with Lee. These issues are fairly pressing and this is a crucial time to discuss them given the immenent closing on the Cubs deal and the timing of our meeting with Lee. Also, I feel like we are not making the best use of her time with us. So, I’m wondering if you might be able to shorten up any of your agenda items (pretty much all items between 9am and 1pm). For example, can we shorten the economist talk or have it during a conference call at another time? That would free up another hour to make use of Lee’s expertise. Please give it some thought. Thanks.

Love,

Laura

Joe was was receptive to the suggestion, but also made sure to remind Laura just how much the guest economist was costing him:

Well, my personal opinion is that Mukesh (the economist) is more important in this meeting than Lee. I’m paying him $25,000.00 to come for the hour. Understanding the economic issues is part of my estate planning process. I’ll explain more at the meeting recognizing that you may not agree.

I don’t know what the family dynamic issues may be, however, if you would like to cancel the issues that I have on the agenda I would be happy to put them off until next time and give you this time to go over the things you think are necessary with Lee. Just let me know what you want to do.

February 27, 2009

Levitt sent an email to the group working on the Cubs deal with a brief update on various issues, including MLB’s stance on the huge amount of debt the Ricketts needed to take on in order to complete the purchase:

MLB Status Call. Schedule a call with Brent, Mary Kay, Nils, Dave, Tom (?), and me where we bring them up to speed on where we are with MLB and how we see the process. It is clear they have not focused on the MLB process and appear comfortable largely deferring to us. Dave was extremely pleased to hear that MLB has heard the $550mm debt number and did not freak-out. He is also happy to hear that we have begun to socialize our capital structure with them. Dave is checking with Nils and will propose potential times for this discussion.

All the fretting over MLB’s debt service rule that the family’s lawyers did back in July 2008 was apparently unfounded.

March 18, 2009

The family finally got an update from Tom about how negotiations with the Tribune were going:

CONFIDENTIAL.

Family,

The last couple of days of negotiation with the Trib have moved the ball forward significantly.

While not all issues have been resolved, we think we have identified the key deal terms and are working toward a quick resolution

With respect to material economic terms, we potentially received some cash concessions to offset our negative surprises in due diligence and held firm on our positions

With respect to documentation issues, some docs are closer to completion than others but we made real progress on all fronts.

We can discuss in more detail on the Friday call.

May 7, 2009

After more than a month of additional negotiations, the Ricketts sent over their first term sheet to Nils Larsen at the Tribune. Tom forwarded his email to Nils to the rest of the family to let them know that the deal was near the finish line:

Hey Nils,

Good to catch up today. Here is the term sheet that will get this deal done. Let me know when you would like to discuss.

Tom

The term sheet saw the Ricketts knocking the price down from their revised bid in January. The final offer put a headline value of $820 million on the Cubs, and planned for the family to finance the purchase with $450 million of debt:

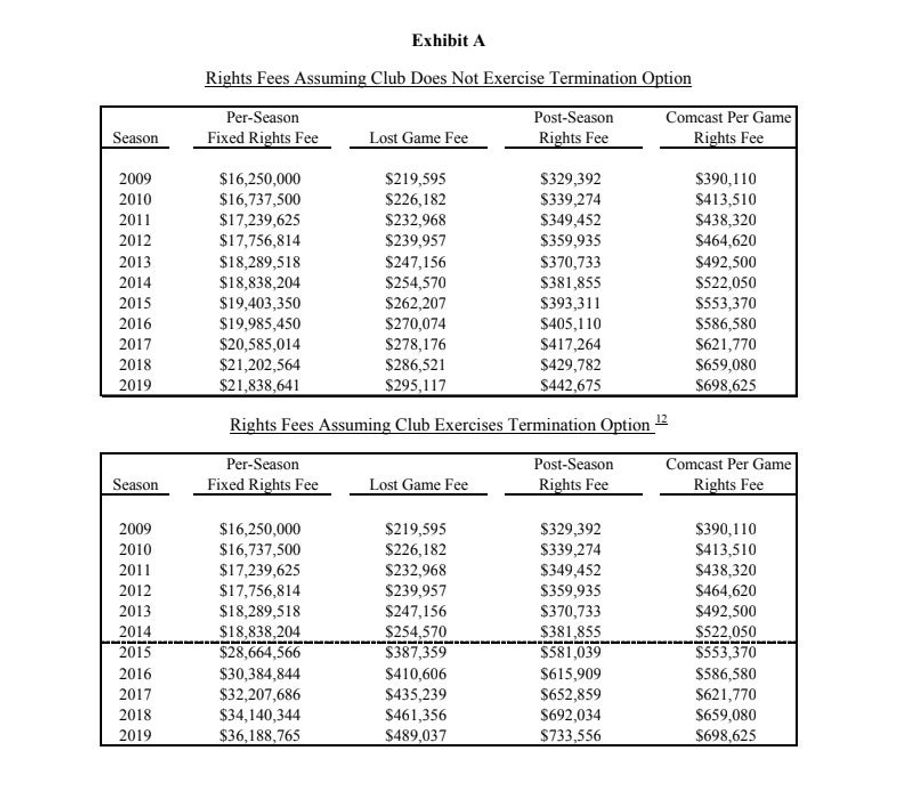

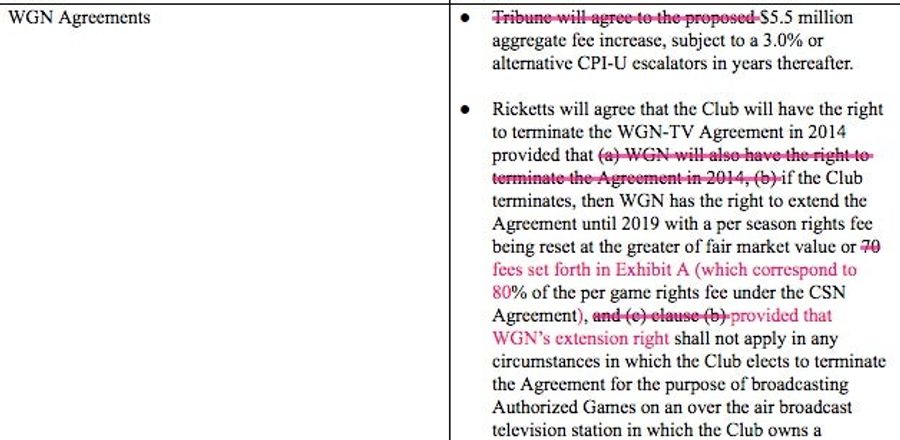

The term sheet also tweaked the details of the WGN deal that were proposed in January. Instead of asking for a $5 million aggregate rights fee increase and a team opt-out in 2014, the Ricketts asked for a $5.5 million aggregate increase and an opt-out that, if exercised, would give WGN the ability to renew the deal for five years at a “fair market value” or a rate equal to 70 percent of the rights fees paid to the club by CSN. The sheet came with a table outlining how much more money the Cubs stood to make if the opt-out was exercised:

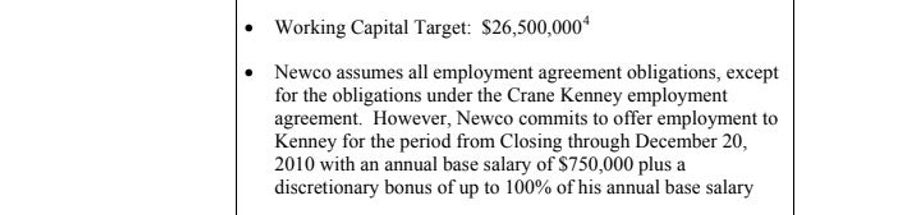

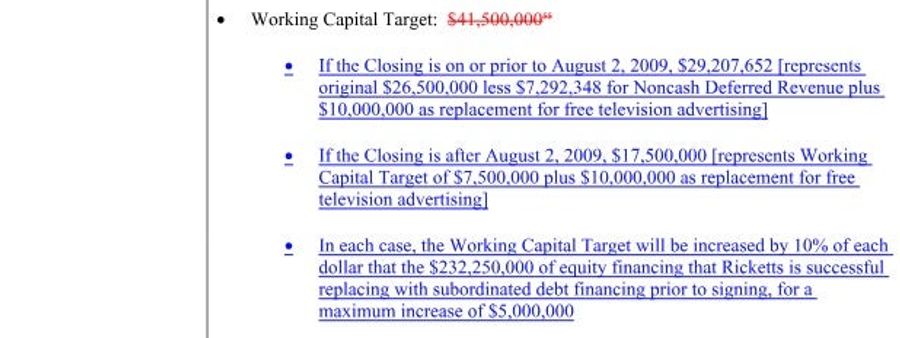

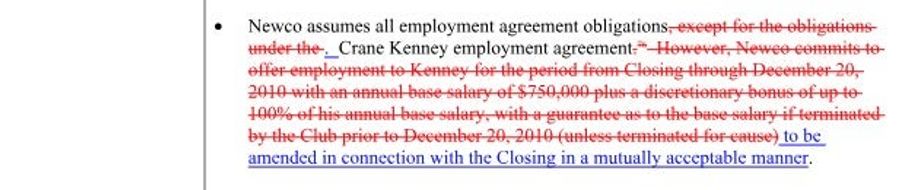

The term sheet also included two other proposals that would go on to become contested issues. The first was a stipulation that the working capital target for the newly formed partnership owning the team would be $26.5 million, and the second was that the Ricketts would not be required to pick up Crane Kenney’s contract:

The working capital target is often a source of tension in big acquisition deals. In accounting terms, working capital is a company’s current assets minus its liabilities, but during an acquisition it becomes something of a moving target. The seller and buyer need to agree on a working capital target—essentially how much cash the seller will leave the buyer once the sale is completed—and the seller can adjust that number up and down by juggling various assets and liabilities before the sale in ways that affect the company’s future cash flows. The Ricketts explained how they landed on their $26.5 million in a footnote, which came along with a warning that any reduction in the target would have to come with a reduction in the headline value of the bid:

May 8, 2009

Tom Ricketts and Nils Larsen had a phone call to discuss the term sheet that the family had sent over the previous day. Tom circulated his notes from the call to the rest of the family, and they indicated that Larsen was not pleased by the precipitous drop in the club’s valuation:

I spoke to Nils.

My notes:

- He appreciated the ‘self-explanatory’ nature of the term sheet but it is a fairly significant move in value that needed to be thoughtfully reviewed.

- He said that MWE would reach out to Foley to discuss some terms and address our “multiple inherent inconsistencies in the draft”.

- JPM would work to understand the “migration of value” over time to understand and make sure they are not missing anything.

- He was….drum roll please…”surprised and disappointed by our lack of willingness to consider the preferred concept”

- He says that he constituents “bear the full hit” of the financing issues (I told him he was wrong on this and to look to our many economic gives).

- His initial response was to keep going and come back with something or “maybe we are just too far apart…I haven’t decided yet”.

There is more but basically he said he would get back to us next week.

GSP- will you set up a call for Monday morning please.

Tom

May 29, 2009

On May 16, the Tribune sent the Ricketts a new term sheet that raised the headline value of the franchise back to $876,300,000. The Ricketts considered this, and two weeks later they circulated among the family a redlined version of the Tribune’s term sheet to be considered as a potential response.

The redlined term sheet had the Ricketts accepting the increased bid value:

But the family sought concessions elsewhere in the agreement. One thing they wanted to do was sweeten the terms of WGN agreement by removing WGN’s ability to opt out of the deal and raising the price of the team’s opt-out rights fees from 70 percent of the price of the team’s deal with CSN to 80 percent:

They also wanted to bring back a term that had been in their revised bid from January 9, which would have required WGN to provide a set amount of free advertising air time to the Cubs:

June 17, 2009

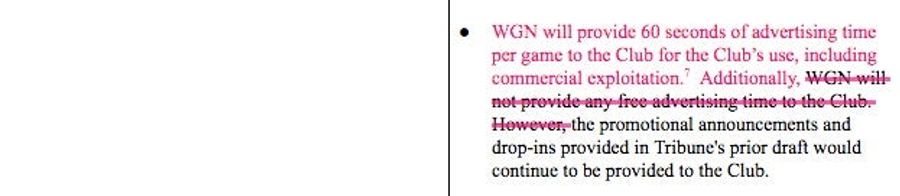

After another few weeks without an update on the negotiations, the family finally received an email from Tom laying out where things stood. At this point, the family was able to secure a team opt-out rights fee worth 75 percent of the CSN rights fee, but wasn’t able to get WGN to provide free advertising for the club. The email also hinted that there could still be future disagreements over the working capital target on the horizon:

Dear Family,

Just got off a call with the deal team. The response from the Tribune is thought to be fairly reasonable and give us hope that they are actually trying to close and not just stall for time.

The highlights:

1. the document is lightly marked. In other words, unlike past term sheets, they have accepted most of our language, formatting, key issues, etc.

2. they have made some economic concessions

a. they have agreed that should WGN wish to extend the TV contract beyond 2014 they would- these represent $12.5mm in NPV to us

i. pay 75% of what the team is receiving on Comcast (as opposed to initial 70% bid)

ii. pay the “Superstation Fee” that is currently paid by the team $3mm/year (as opposed to us paying it)

iii. WGN does not have the right to extend if we have our own TV station.

b. they have extended the final maturity of the seller financing (preferred) and put right from 4 years to 9 years

c. they increased the Net Op Income adjustment cap from $15mm to $20mm – this is a net positive of $5mm to us at close

2. they did not give on TV commercials (“avails”)

The other shoe to drop at this point is that the Tribune is reviewing the Net Working Capital amount. They did not take out our $26.5mm number but they have not confirmed it either. This is cash left at the team at close and has been somewhat of a windfall for us as did not budget it in our January bid.

I will keep everyone posted if anything happens of significance today.

June 27, 2009

Shit started to hit the fan. The Ricketts sent a revised term sheet to the Tribune on June 20, and a week later they received a redlined sheet in response. They did not like the response. Levitt sent the following email to the family:

The Tribune responded last night to the Term Sheet. Tribune’s redline is attached. The response was unacceptable and represented a significant departure from the discussions that have occurred this week with Nils. Rather than to prolong this process, we made the judgment last night to reach the bottom-line. Accordingly, Tom sent an email rejecting the Tribune’s proposed revisions to the Term Sheet with the exception of agreeing to (a) work to move $50mm of equity into sub-debt, and (b) strike the “or cable” provision from the WGN extension paragraph. In all other respects, Tom reverted back to the family’s most recent proposal but imposed a deadline of Wednesday at 5pm CT at which point the offer would terminate. On a parallel track, we are back channeling to MLB our position. Additionally, early next week, we will back-channel to the Tribune’s creditors our position so we can bring maximum pressure to bear on Tribune.

Joe responded, calling the the Tribune the “most foolish and irresponsible negotiators” he had ever witnessed:

I like the fact that the deadline has been set. At that time we either do it or we are finished.

The tribune needs to know that we are ONLY buyers on the terms we gave to them. If these terms are not acceptable then the Tribune needs to find a buyer that will give them what they want.

You are correct, that in the mean time, the Creditors need to know what they will be losing.

The Tribune is the most foolish and irresponsible negotiators I have ever witnessed or experienced.

J. Joe Ricketts

Looking at the redlined term sheet, it’s easy to pick out some of the Tribune’s responses that got the family so riled up. The Ricketts had been willing to forgo the free advertising spots on WGN in exchange for a higher working capital target, and their term sheet explicitly stated that one was a trade for the other. The Tribune put a big red line through that, and in response proposed a much lower, and shifting, working capital target:

Further down, the Tribune’s response also reinstated the requirement that the Ricketts pick up Crane Kenney’s contract:

The Ricketts had also added an item to the term sheet that would have restored their exclusive negotiating window with the Tribune, which had been granted in January but had since expired. This was a big ask by the Ricketts, because Marc Utay, the private equity mogul who Joe and Levitt had previously deemed not to be a threat, had re-entered the bidding process and was pushing hard to acquire the team. The Tribune’s response indicated that they were not interested in re-establishing exclusive negotiations:

Tom later sent an email of his own to family, expressing his own dissatisfaction and his response to Nils Larsen:

Family,

Below is the email I sent to nils.

His counter represents opening a whole new discussion on Net Working Capital that represents a $19mm new, net price increase for us.

I think we all agree that this has to end somewhere and maybe this will help. (My real believe is that the arrogance of the Tribune will make them to ignore our deadline)

We will hit the ground running next week with calls to the proper individuals that will help make our case to creditors.

Here we go.

Tom

Nils,

After looking at this again I really don’t think I need to wait until Monday to respond. This Term Sheet is a significant step backwards after some real progress.

Our position going forward is very simple:

- We will work in good faith to shift $50mm of what had been equity into sub debt, provided the rating agencies and our lenders agree.

- We will agree to your proposed change in the second bullet of the WGN agreements section of the Terrn Sheet, striking the words “or cable”.

- In all other respects, the offer we transmitted on June 20 is unchanged and remains open until Wednesday, July 1 at 5pm CT. After that time, our offer is withdrawn.

This has been a very long process but we have reconciled ourselves to the fact that, despite our best efforts, we may not be successful in reaching terms that work for both the Tribune and the Ricketts family.

Tom

Joe suggested that maybe it was time to walk away from the deal altogether:

I agree. It is time to walk away.

June 30, 2009

The Ricketts whipped up yet another term sheet to send to the Tribune, and Tom sent an email to the family updating them on where things stood:

Dear Family,

Attached is the latest term sheet.

I spoke to nils yesterday and believe that the Trib understands our position. We are currently taking the avails as a purchase price reduction 876 - 861 for the TV avails and other concessions are built into working capital cash at close of $45mm. In the end I believe this is roughly a “real price” of $815mm vs the $900mm from January.

We are still pushing for some closure tomorrow.

“Avails” is shorthand for the free WGN advertising slots that the family had initially asked for—Tom is saying that he agreed to trade those away for a reduction in purchase price and a better working capital target.

July 9, 2009

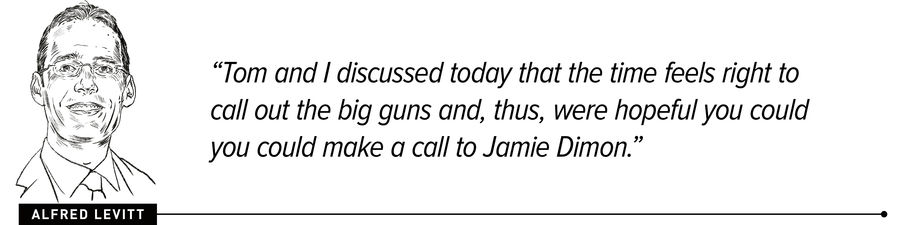

The Ricketts’ July 1 deadline came and went, but negotiations continued. Joe received an email from Levitt explaining that the Tribune and the family had yet again failed to come to an agreement, and theorized that the company was sandbagging in order to buy time for Utay to increase his bid. Levitt suggested the family respond by making a tactical move of their own: complaining to JPMorgan CEO Jamie Dimon:

Joe –

As you correctly predicted, Tribune did not sign the non-binding Term Sheet or Fee Reimbursement Letter yesterday. While they are not attempting to renegotiate any economic terms – as you directed, Tom has made plain that economics are not on the table – they continue to haggle over certain mechanics. While some of what they are seeking is acceptable, the unending negotiation suggests that they are either incapable of closing a deal or delaying for tactical reasons – e.g., to afford Utay an opportunity catch-up to the family’s position. (Our market intelligence as of late as last night indicates that Utay is still out of the picture, but we have to take all that with a large grain of salt.)

Tom and I discussed today that the time feels right to call out the big guns and, thus, were hopeful you could you could make a call to Jamie Dimon. As one of our lenders, the largest creditor of Tribune, and Tribune’s financial advisor on the trade, Dimon is well positioned to force some sanity on this process.

We suggest the following three basic points to Jamie Dimon:

1. Dysfunctional Negotiation.

a. The Ricketts have $450mm in senior debt lined-up, all our equity sitting in cash, Baseball signaling that they’ve signed-off on our deal and our ownership, but we still can’t get these Tribune guys to stop negotiating every little term.

b. I’ve done a lot of deals, but this is the most screwed-up deal I’ve ever seen.

2. Out of Patience.

a. I’ve stayed in this deal for longer than I otherwise would have because my kids wanted the team, but I’m nearing the end of my patience.

b. I will pull the plug within days if I don’t feel that there is a clear path to closing on the terms we have proposed.

3. Creditors Will Be Hurt.

a. If we walk, it’s the creditors, like JP Morgan, who will be hurt so I am not even sure why we’re still talking to Tribune.

b. I felt that I owed you this courtesy heads-up.

I’m about to hop a plane to Omaha, but perhaps you, Tom, and I could visit briefly by phone later to discuss this plan.

It’s unclear if Joe ever had a conversation with Dimon; neither Joe nor Levitt responded to a question about whether this planned conversation ever happened. But just hours after Levitt made his suggestion, negotiations were suddenly progressing again, according to an email from Tom to the family:

As Dad predicted, we did not sign a term sheet wednesday. However, we have ironed out the last wrinkles that they put in and are, again, moving forward.

As of this afternoon, Nils sent the Term Sheet and Fee Reimbursement Letter to their Creditors Committees and let them know he intends to execute them..

Both sides will sign the docs in the morning and then it is our intention to execute bank commitment documents.

Moving forward....

Tom

July 11, 2009

Just two days, later a deal was reached, and Levitt sent along the good news:

Team Ricketts -

Yesterday, Tribune signed the non-binding Term Sheet and $3.5mm Fee Reimbursement Letter. Following that, the Education Trust signed the documents to secure the $450mm in senior commitments.

Later today, we will circulate the signed Term Sheet and updated sources and uses materials.

The legal teams are now driving hard toward exchanging the next set of definitive deal documents.

In other news, we believe the press will be running a story about the Cubs having to be put through bankruptcy as part of the transaction. Our PR strategy is to stay clear of this story until we have definitive documents signed but we’re coordinating closely with MLB on this issue.

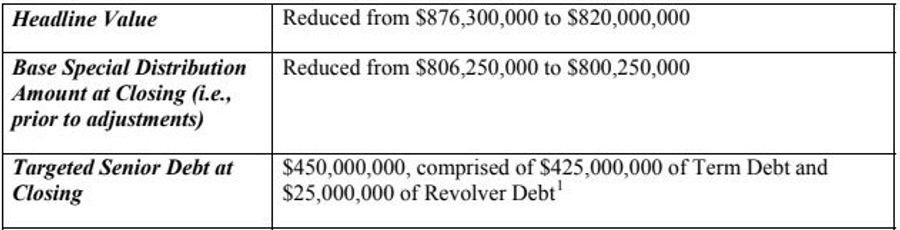

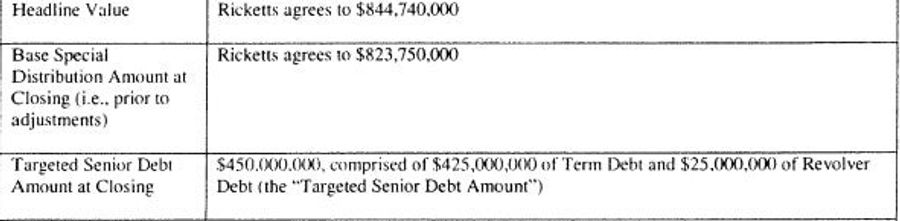

The final, executed term sheet had the Ricketts and Tribune settling on a headline value of $844,740,000, to be funded by $450 million in debt:

The Ricketts did not ultimately get any free advertising spots from WGN, and did agree to to pick up Crane Kenney’s employment contract. They did get a more favorable working capital target, though, and the opt-out clause that would allow them to renegotiate their rights fees with WGN. The Cubs did eventually take advantage of the opt-out, and signed a new five-year deal with WGN in 2015 to broadcast 45 games per season. That same year, the Cubs signed a five-year agreement to broadcast 25 games per season on ABC 7. The rest of the games would continue being broadcast on the NBC Sports Chicago (formerly CSN), the regional sports network in which the team owned a 25 percent stake along with the Bulls, Blackhawks, and White Sox. All of those deals are set to expire in 2019, and the Cubs are currently trying to create their own television station, reportedly in partnership with right-wing media company Sinclair Broadcasting.

July 31, 2009

Tom sent an email to Joe letting him know that he was still locked away trying to finalize the purchase with the Tribune’s lawyers, and that he needed some extra money from mom and dad:

Dad,

As you may know, we are sequestered with the Tribs lawyers. We have made some good progress but there is new issue.

We have represented to the Tribune that we will have a back up fund of $20mm available should we do anything that creates a tax liability for them and theteam does not have the resources to cover the cost. Up to this point, we have assumed that a Dynasty Trust could stand in for that obligation. As we have been advised this moring by our estate counsel, it is not possible the Trust to simply issue a guarantee of this sort. We discussed many options but the two that work are:

1. The trust makes a distribution of some sort to the siblings (or some form of loan) and then the cash is kept in an account for the life of the obligation. This is workable but complicated and takes liquidity out of the trust.

Or:

2. Have mom sell shares to cover the $20mm. She would then keep the dollars in high grade securities until the end of the term of the obligation. This is simple but requires more shares to be sold.