Cleveland Cavaliers Owner Dan Gilbert's NBA Championship Is Nothing To Celebrate

Hundreds of thousands of people crowded downtown Cleveland on Wednesday to celebrate the Cavaliers’ NBA championship, and aside from the 15 million or so people in Northern California, it seemed the rest of the country was celebrating alongside them—and rightly so. The Cavs took down the heavily-favored, shit-talking Warriors, won Cleveland’s first championship in 52 years, and brought real happiness to a city that’s known hard times.

For all that, there is one very legitimate reason to be disappointed the Cavaliers won a championship: It means Cavaliers owner Dan Gilbert won too. As much as the Warriors and their trophy-fucking owner get made fun of around here, Gilbert’s sins extend far, far beyond writing the sports equivalent of a runaway slave letter to LeBron James in comic sans. He is a bad man whose companies have helped destroy large swaths of largely poor and largely minority urban areas, and he should be held in contempt, not celebrated.

What Lawsuits Reveal About Quicken Loans’ Lending Practices

Dan Gilbert made most of his fortune through owning Quicken Loans, which has grown to become the country’s largest online mortgage lender, and third-largest mortgage lender overall. In getting there, Quicken engaged in many of the same predatory lending practices that precipitated the 2008 financial crisis, and has been the subject of numerous lawsuits across the country, in which some of their heinous lending practices have been laid bare.

The best-known case is that of West Virginians Lourie Jefferson and Monique Brown, who won an almost $3 million total judgement against Quicken (after years of appeals over the amount of the judgement, Quicken “settled for the full verdict that came to nearly $2.7 million with interest,” according to Jefferson and Brown’s lawyer). The judged ruled Quicken’s actions to be legally “unconscionable,” and found that the company committed fraud and violated the West Virginia Consumer Credit and Protection Act when it, among other things, failed to properly disclose that Jefferson and Brown’s loan contained an outrageous provision for a balloon payment of $107,015.71 to be paid at the end of 30 years. That wasn’t all, according to the :

At the first phase of the trial, the Court ruled in favor of Jefferson and Brown on numerous counts. The court found the lending practices of Quicken Loans unconscionable, based in part on Quicken’s utilization of a highly inflated appraisal in making the loan.

The court also found that Quicken Loans defrauded the homeowners by misleading them into paying excessive loan origination fees; falsely promising to favorably refinance the loan in the near future; and concealing an enormous balloon payment from its own borrowers.

In another case, Quicken settled with the Federal Deposit Insurance Corporation for $6.5 million for allegedly selling “soured loans” (Quicken did not admit to wrongdoing), and then told the they didn’t believe the settlement would be made public:

Quicken Loans spokeswoman Paula Silver expressed surprise that the settlement became public, saying officials at the lender had believed that would not occur. “Quicken Loans and the FDIC entered into a ‘confidential’ agreement nearly three and a half years ago which clearly states that no party admits liability nor wrongdoing,” Silver said in a statement.

The biggest blow to Quicken’s self-professed image of squeaky-clean lending processes is potentially yet to come, though. Last year the federal government sued Quicken Loans for allegedly underwriting hundreds of Federal Housing Administration-insured loans in ways that violated the False Claims Act. The case will likely take years to resolve; should Quicken lose, it could cost the lender hundreds of millions of dollars. ( Gilbert has said the government is seeking a “nine-figure settlement,” and denied the charges.)

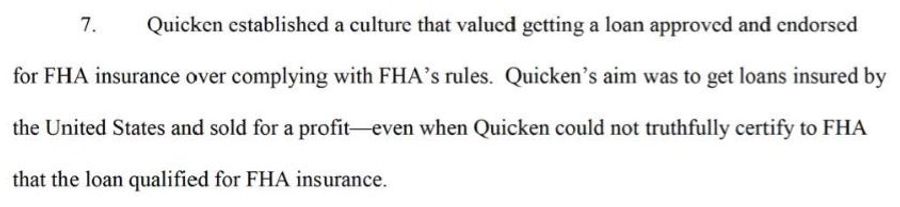

The government’s initial filing ( PDF) makes clear that it believes Quicken’s alleged misdeeds run deeper than just an employee or two, but rather stem top-down from the company’s culture:

It is an incredible document, with the government alleging many things even a layman can understand Quicken shouldn’t have done: approving a loan even after the borrower asked for a refund of the mortgage fee to feed her family; approving a loan for a second residence, in clear violation of FHA rules; and approving a loan for a borrower who told them he was close to bankruptcy.

To approve these loans, the government says, Quicken used a number of tricks to approve loans in ways that were not FHA-compliant, resulting in “millions of dollars in existing losses to HUD” when borrowers defaulted, and likely “significant additional losses to the agency” in the future. The press release announcing the lawsuit described them this way:

For example, Quicken allegedly had a “value appeal” process where, when Quicken received an appraised value for a home that was too low to approve a loan, Quicken often requested a specific inflated value from the appraiser with no justification for the increase– even though such a practice was prohibited by the applicable FHA requirements. Quicken also allegedly granted “management exceptions” whereby managers would allow underwriters to break an FHA rule in order to approve a loan.

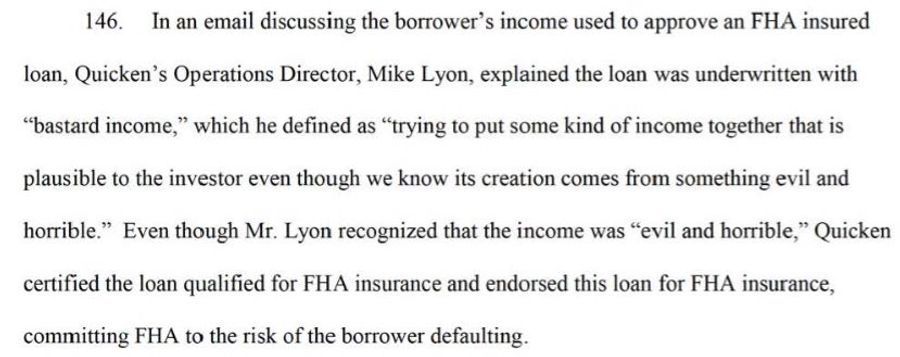

The filing also contains damning quotes from emails allegedly sent by senior Quicken executives. For instance, one exec allegedly sent an email acknowledging that Quicken approved loans underwritten with what they called “bastard income”:

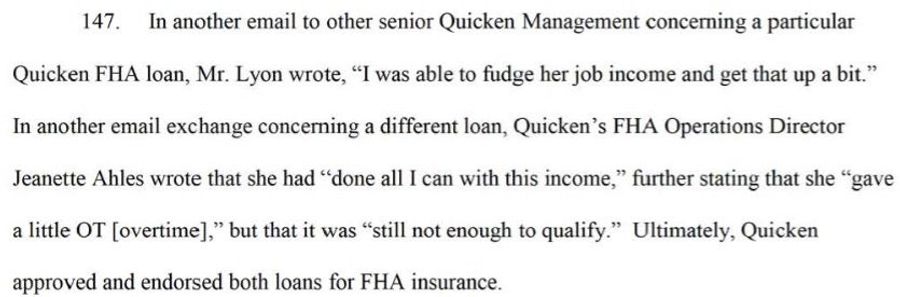

In other emails, Quicken execs allegedly copped to fudging income and approving loans for borrowers who didn’t qualify:

The Culture Of Quicken Loans

Quicken Loans regularly touts its placement on lists of the best places to work, but some former employees tell a very different story. Quicken has faced a number of lawsuits about unpaid overtime pay for mortgage loan officers, as whether they qualify for overtime or not is very complicated. (In 2015 the Supreme Court ruled that mortgage loan officers were eligible for overtime pay, though Quicken said this ruling would not affect their employees.)

In the largest overtime pay class action lawsuit—covering hundreds of former employees—to go to trial to date ( Quicken won), former employees described a wide range of deceptive behaviors. According to a Center For Public Integrity report, one former Quicken salesman said in a sworn statement that he and his colleagues increased profits by “locking the customer into a higher interest rate, even if they qualified for a lower rate, and rolling hidden fees into the loan.”

Another former Quicken employee explained in court papers how she screwed over a customer with cancer:

She recalled selling a loan to a customer who had cancer and needed cash to pay medical bills: “I could have offered him a home equity line of credit to pay these bills but, instead, I sold him an interest-only ARM that re-financed his entire mortgage. This was not the best Quicken loan product for him, but this was the one that made the company the most money.”

Numerous former employees also described in court papers a common technique that basically amounted to extorting customers to do business with Quicken:

One way that Quicken hustled borrowers, several former employees said, was a sales stratagem known as “bruising.” As one former employee described the technique, the goal was to “find some bad piece of information on their credit report and use it against them, even things as insignificant as a late credit card payment from several years ago. Quicken’s theory behind this was that if the customers can be scared into thinking that they cannot get a loan, then they will be more likely to do business with Quicken.”

What happened, and happens, at Quicken takes place within a company that has been described as “Scientology-esque.” Quicken is obsessed with ISMs (like the suffix), which they call “the foundation and the philosophy that we live by.” In something straight out of a Silicon Valley parody or Jason Whitlock’s playbook, the ISMs are a series of meaningless business maxims like “A penny saved is a penny” (i.e., instead of scrimping, spend your time trying to earn dollars) and “We are the ‘they.’” Just read this very, very creepy blog post from a Quicken intern.

Disgruntled former Quicken employees have described their role as trained monkeys; one described the work environment as “very hostile, with management using intimidation tactics, public humiliation, and profanity when dealing with the sales team members.” It probably goes without saying that Gilbert is fiercely anti-union, and the National Labor Relations Board ruled earlier this year that six of his companies included illegal, threatening anti-union language in company handbooks.

Quicken’s Argument

Gilbert and Quicken Loans have always maintained that the vast majority of their products are “vanilla” loans, challenged the definition of subprime mortgages, and repeatedly asserted that Quicken didn’t sell subprime loans. But in 2007, before the financial crisis, none other than Quicken’s CEO told CNN that two percent of the company’s business was in subprime loans. And a Detroit Newsof loan records found, going by one common definition of what constitutes a subprime loan, that 24 percent of Quicken’s loans in the city of Detroit between 2004 and 2006 were subprime.

An important caveat is that there is a reason Quicken Loans still exists and is thriving, while former competitors like Countrywide and Ameriquest Mortgage went under. However we define subprime loans, Quicken originated far fewer of them as a percentage of their business than other lenders. An industry analyst summed things up to the Detroit News, though, “Quicken would argue their track record was better than anyone in the industry, but of course the bar isn’t that high in the mortgage industry.”

Transforming Detroit Into A Robocop -Like Playground For The Wealthy

Besides running a company that has been repeatedly sued for its lending practices, Gilbert is at the heart of “revitalizing” Detroit. He has bought at least 70 downtown properties for comically low prices, convinced the state of Michigan to give him at least $50 million in tax breaks ( some put the total tally as high as $200 million) to move Quicken’s headquarters from suburban Livonia into Detroit by threatening to move out of state, and runs what amounts to a shadow private police force.

Gilbert’s Rock Ventures—the holding company for his numerous business ventures—employs hundreds of security guards and has installed over 500 security cameras in downtown Detroit, and the entire operation is run out of a Las Vegas casino-like security war room in one of his buildings. Rock Ventures doesn’t like to talk about this quasi-police force (though after sustained criticism they did let a reporter tour the security center), and of course they aren’t subject to any of the usual laws or even norms that governs the public’s right to obtain information on and demand oversight of the police. Rock Ventures takes this so seriously that they’ve installed their cameras on other people’s property without permission. (Gilbert called the journalist who first reported the story “dirty scum.”)

Gilbert’s companies aren’t the only downtown business to employ security forces, but his is by far the largest, effectively supplanting the police across a huge area, and by far the most secretive. But beyond the justified concerns about privacy and surveillance, the security force is just one piece in Gilbert’s plan that would make certain parts of Detroit a RoboCop-like playground for the upper middle class and rich, at the expense of the poor.

Dan Gilbert & Warren Buffett talk at an invite-only “Detroit Homecoming” event. (Photo credit: Bill Pugliano/ [object Object] )

Dan Gilbert & Warren Buffett talk at an invite-only “Detroit Homecoming” event. (Photo credit: Bill Pugliano/ [object Object] ) Gilbert’s real estate wheeling and dealing has received fawning press coverage, but it’s not clear why. A long Mother Jones piece reports that the Blight Task Force Gilbert co-chaired—that in itself is ironic, given that Quicken originated the “fifth-highest number of mortgages that ended in foreclosure in Detroit over the last decade”—recommended tearing down 70,000 properties, but didn’t endeavor to find out how many people actually lived in those properties, nor develop a plan to help relocate those residents. According to Mother Jones, at a White House meeting that resulted in almost $150 million in blight removal funds for Detroit, it “appears that not a single representative of the neighborhoods soon to be bulldozed ... attended the meeting.” (A Wayne State University professor called it “the suburban view of what a city should look like” and added “it’s not a view of the city that’s responsive to the needs of the citizens of Detroit.”)

Gilbert and people like Red Wings owner Mike Ilitch—who got hundreds of millions in public financing for a new downtown arena literally the week after Detroit underwent the largest municipal bankruptcy in United States history—would remake Detroit into a city that is accommodates the needs of the relatively privileged few at the expense of the numerous poor. One of the best examples of this boondoggle is the M-1 Rail.

As originally conceived, the M-1 Rail would’ve been a 20-mile long streetcar line that would connect northern Detroit suburbs to the downtown core. But it is instead being built as a less than four-mile long line that will run between downtown and the gentrifying midtown. As Mother Jones reported, a quarter of Detroit households don’t have a car, and could really use a robust public transportation system. Instead they’re getting “a shuttle between jobs they can’t get and housing they can’t afford.”

At least the M-1 Rail’s $180 million cost is mostly being borne by corporations and nonprofits, rather than by public dollars Detroit doesn’t have. To its backers, this is evidence of the commitment Gilbert and co. have to the city of Detroit, and M-1 proponents deflect criticisms of the project by saying it isn’t their job to solve all of Detroit’s problems. To the extent that this is true, it just makes clear that Gilbert’s actions wouldn’t actually regenerate Detroit, but would regenerate Detroit for a very specific kind of person: the kind of person who can live and work in the buildings Gilbert owns.

Gilbert’s investments, blight removal crusade, streetcar project, and Orwellian shadow police force all result in people paying him rent, and corporations leasing offices in his buildings. They’re investments that make money—just like taking advantage of cancer patients refinancing their mortgage—not examples of high-mindedness. As professors Joshua Akers and John Patrick Leary write in a bruising piece for Guernica magazine, “Tycoons of an earlier era had to pursue something besides their main hustle to earn the laurels being heaped on Gilbert. [...] He is portrayed as a Detroit benefactor simply for doing what he does: run mortgage and real-estate companies.”

Dan Gilbert’s Self-Image

To fend off as much negative coverage of his activities as possible, Gilbert takes an extremely hostile line with the press. He makes transgender barbs about reporters he doesn’t like, sends “vile emails” to newspaper executives, leans on brand partners to delete posts with innocuous jokes, and is notorious for sending (allegedly drunken) angry late-night emails to reporters. And those are just some of the known incidents that have been reported.

Rather than embodying the 21st century version of the great American figure of the businessman-philanthropist, like Andrew Carnegie, Gilbert is a thin-skinned weasel who practices a predatory form of capitalism. The worst thing about the Cavaliers’ title? It gives Gilbert one more tool with which to burnish his reputation.

(Photo credit: Ronald Martinez/ Getty)

Related

Why the NBA's New Anti-Tanking Ideas May Backfire

New England Patriots Have Major Needs After Super Bowl Loss

Why the AFC North Makes Sense for Tyreek Hill’s Next Team

- College Basketball Thursday Picks: Feb 19th Best Betting Predictions

- Genesis Invitational Best Betting Picks: Scottie Scheffler Headlines Return to Riviera

- NBA Betting Picks for Thursday Feb. 19th’s Return From All-Star Break

- Best 2026 American League Central Season-Long Future Betting Predictions

- Tuesday Feb. 17th College Basketball Betting Picks and Predictions

- Best 2026 American League East Season-Long Future Betting Predictions

- Best College Basketball Bets for Monday: Duke vs Syracuse, Houston vs Iowa State